The Complete Guide to Building a Pitch Deck That Raises Capital

A comprehensive breakdown of what makes a pitch deck work — from the 10-slide structure to investor psychology, design principles, and common mistakes. Written for founders actively fundraising.

Your pitch deck is not your business. It's a sales document designed to do one thing: get a meeting. Founders who forget this waste months perfecting slide animations while investors swipe through their deck in 47 seconds and move on.

This guide covers what actually works — the structure, the psychology, the design, and the mistakes that kill deals before the first handshake. No fluff, no guru nonsense. Just what separates decks that raise rounds from decks that get archived.

The 47-Second Rule: How Investors Actually Read Decks

The average partner at a venture firm spends 3 minutes and 34 seconds on a deck they like. On one they don't? Under a minute. That's the window you're working with, and that window is shrinking. Mobile-first reading habits mean investors are swiping through your deck on their phones between meetings, and they make a keep-or-delete decision in the first 3 slides.

Scanning Before Reading

Investors scan in a Z-pattern — top left to top right, then diagonally down to the bottom left, then across to the bottom right. Your most important information needs to live in those hotspots. Headlines, not paragraphs. Numbers, not adjectives. Every slide should be legible in 5 seconds at arm's length. If an investor has to squint or lean closer, you've lost them.

The rule of thumb: if you can't read the key message from a slide while holding the phone at arm's length, the font is too small or the slide is too busy. This is the single easiest fix in most decks, and almost nobody does it.

The Pre-Read Filter

Most investors pre-scan decks on their phone — in an Uber, between meetings, during a kid's soccer game. If your deck doesn't communicate the core thesis in the first 3 slides on a 6-inch screen, it's getting passed to an associate, which means it's getting filtered. Design for mobile first. Desktop is a bonus, not a requirement.

This means: one idea per slide. Large headlines that tell the story without needing the body text. Visuals that explain concepts in a glance. If your deck relies on reading every word to be understood, it's going to fail the pre-read filter.

The Forward Test

The only metric that matters when reviewing your deck slide by slide: does this slide make the investor want to see the next one? If any slide stops momentum — too dense, too confusing, too boring — it's a leak. The investor doesn't toss the whole deck. They just stop reading and move on to the next one in their inbox.

A deck that passes the forward test gets read to the end. A deck that fails gets an email template rejection or, more commonly, silent disinterest. Test this: send your deck to five friends who know nothing about your space and ask them to read it. Watch where they slow down. Those are your leaks.

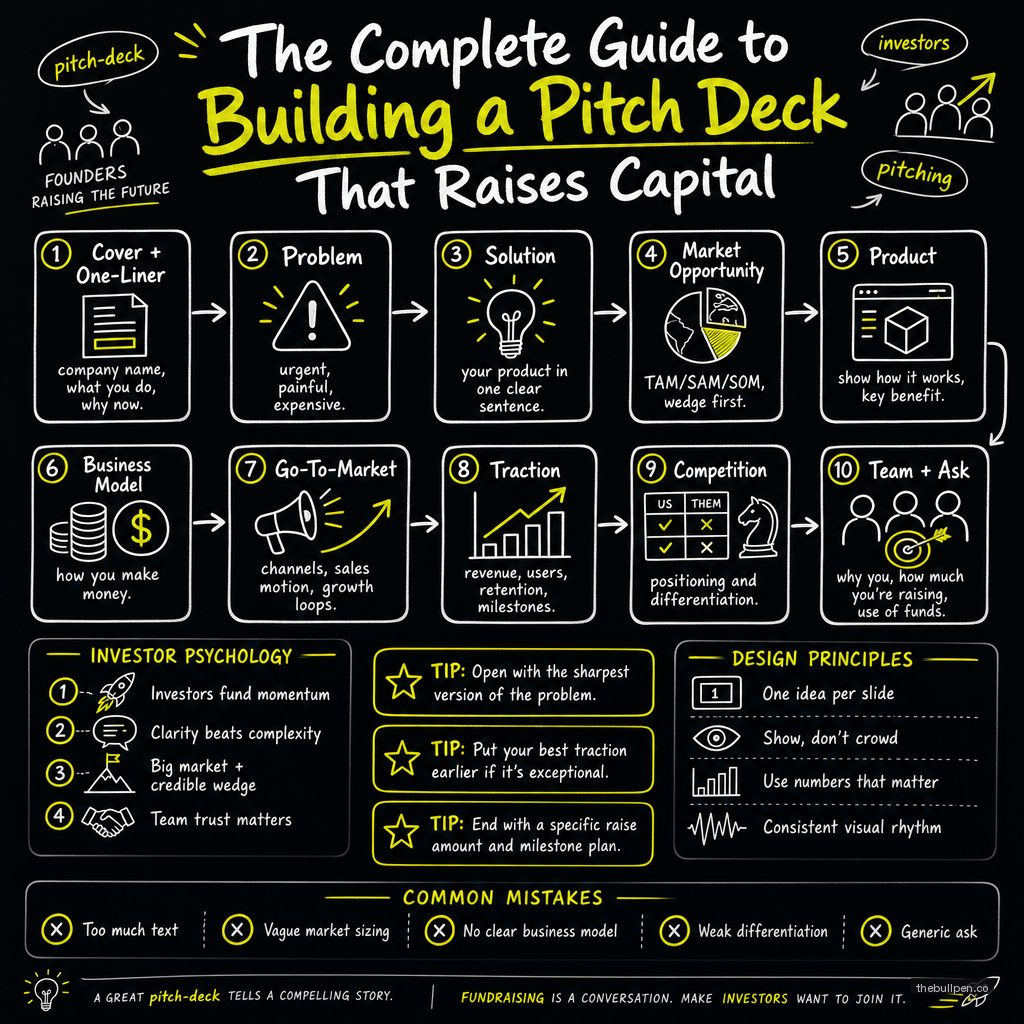

The 10 Essential Slides

There are exactly 10 slides you need. Not 8, not 12, not 15. Exactly 10 for the main deck. Anything that doesn't fit goes in the appendix. Investors have a mental model of what a pitch deck looks like, and deviating too far from that structure works against you. They're looking for information in a familiar order. Give it to them.

Problem

The single most important slide. Investors need to feel the pain before they care about your solution. This isn't about describing a problem abstractly — it's about making the investor nod and think "god, yes, that's real, I've seen that."

Bad problem slides sound like: "Small businesses struggle with inventory management." Every investor has heard that a hundred times. Great problem slides sound like: "Maria runs a boutique with 3 employees. She spends 14 hours a week reconciling inventory across her store, her website, and her Instagram shop. Last month, she lost $4,000 in sales because items she'd already sold were still listed online."

Lead with a specific person or company who experienced this pain. Quantify the cost — time, money, or opportunity. If you can't name a real customer who has this problem and would pay to solve it, you're not ready to pitch.

Related: How to Build a Problem Slide That Hurts

Solution

One sentence. One visual. That's it. Your solution slide should be so clear that a non-technical investor could explain it to their spouse at dinner. If you need more than one sentence to explain what you do, you don't understand your own business well enough yet.

Avoid feature lists. Avoid technical architecture diagrams. Show the before-and-after state. The investor needs to understand what changed for the customer, not how your backend works. A simple split-screen with "Before" on the left and "After" on the right is more effective than any amount of copy describing your product.

Related: Pitch Deck Solution Slide Best Practices

Market Size (TAM/SAM/SOM)

This is the slide where most founders lose credibility. They pull a random CB Insights report, multiply by some arbitrary percentage, and call it their TAM. Investors have seen this a thousand times and they're not fooled by it.

Use the top-down approach for TAM (total addressable market — the global market if everyone who could buy, did). Use bottom-up for SAM (serviceable addressable market — the segment you can actually reach with your distribution). Use your actual pipeline for SOM (serviceable obtainable market — the portion you can realistically capture). If your bottom-up number doesn't match your top-down number within a reasonable range, something's wrong in your assumptions.

B2B founders: anchor on number of companies × average contract value. B2C founders: anchor on number of users × revenue per user. Be honest about constraints. Investors would rather see a realistic $500M TAM with a clear path to capture it than a fantasy $10B TAM with no distribution strategy.

Related: Pitch Deck Market Size: TAM, SAM, SOM Explained

Why Now

Timing is the most underrated slide in any deck. Good ideas at the wrong time fail. Bad ideas at the right time succeed. The history of startups is full of companies that were right but too early. Show why this moment — technologically, culturally, regulatorily, economically — creates an opening that didn't exist 3 years ago.

Maybe AI inference costs dropped 90% in the last 18 months. Maybe a new regulation created compliance demand. Maybe remote work permanently shifted buying behavior in your category. Maybe a generation of incumbents is aging out. If you can't articulate why now, investors will assume you're either too early (and will run out of runway before the market matures) or too late (and someone else will beat you).

Traction

Traction is reality. Everything before this slide is a story — an important story, but fiction nonetheless. Traction is the moment when the investor stops evaluating your narrative and starts evaluating your numbers. It's the most trustworthy signal you can provide.

Pre-revenue: show waitlist signups, letters of intent, pilot agreements, user growth curves, engagement metrics, anything that demonstrates demand. Post-revenue: show MRR, growth rate, gross margin, retention curves, cohort data. Don't cherry-pick one metric and hide the rest — the best founders show a dashboard, not a vanity highlight.

For early-stage SaaS, month-over-month growth rate is the single most important number. If you're growing at 20% MoM or higher, that's the headline. If you're growing at 10%, show the trend — is it accelerating or decelerating? If you're growing below 10% MoM, traction is your weakness and you should focus on growth before fundraising.

Related: Building a Traction Slide That Works for Seed

Business Model

How do you make money? This sounds obvious, but an astonishing number of decks bury this information or make it confusing. Show unit economics — CAC, LTV, gross margin, payback period. Show pricing tiers and the logic behind them. Show the math of how a customer becomes profitable over time.

If you're pre-revenue, show your pricing assumptions and the logic behind them with sensitivity analysis. "We'll figure out monetization later" is a sentence that kills deals on the spot. Investors are not betting on your product — they're betting on a business, and a business needs a revenue model.

Related: Pitch Deck Unit Economics Explained (Coming soon — September 21, 2026)

Competition

The standard two-by-two matrix is fine, but here's the trick: don't put yourself alone in the top-right corner. That's what literally everyone does, and it tells the investor you're either naive or dishonest. Either way, it's a credibility hit.

Better approach: show a competitive landscape with honest positioning. Acknowledge where competitors win. If the competitor has better distribution, say it. If they have deeper pockets, acknowledge it. Your differentiation should be structural — something they can't copy in 6 months — not just "we have better UX" or "we're cheaper." Structural advantages include proprietary data, network effects, regulatory moats, and deep technical barriers.

Related: The Pitch Deck Competition Slide Done Right

Go-to-Market

How do you reach customers? Vague answers like "digital marketing" or "strategic partnerships" don't count. Show specific channels with CAC estimates, expected volume per channel, and realistic timelines to ramp.

The best GTM slides show one primary channel that's already working (even at small scale) and one secondary channel you plan to test. Investors want to see that you understand distribution physics — that you know how to acquire customers efficiently — not that you've listed every possible channel. Five half-baked channels beat zero channels, but one proven channel beats everything.

Related: Pitch Deck Go-to-Market Slide Strategy

Team

Your team slide should answer one question: why is this specific group of people the best in the world to solve this problem? Don't just list logos. Show relevant domain expertise, previous exits (including failed ones — those teach more), and crucially, why your backgrounds connect directly to the problem you're solving.

Investors bet on people first, ideas second. A B+ team with an A+ idea will almost always beat an A+ team with a B+ idea, but an A+ team with structural advantage in the market they know deeply? That's the combination that gets term sheets. Show founder-market fit, not just credentials.

Related: Building a Pitch Deck Team Slide Investors Trust

The Ask

How much are you raising, what instrument, and what will it get you? Be specific. "We're raising $1.5M in a priced round to get us 18 months of runway to reach $3M ARR" is a clear, confident ask. "We're looking for partners who share our vision" is vague and weak.

Show the use of funds — a simple breakdown or chart showing how the money maps to specific milestones. Hiring, marketing spend, R&D, operating costs — each with a percentage and a rationale. Investors need to see that you've thought through capital efficiency. A founder who can articulate exactly why they need $1.5M and not $1M or $3M shows the kind of operational thinking that makes them backable.

Related: Crafting a Pitch Deck Ask Slide That Works

Design Principles That Matter

Your deck doesn't need to be beautiful in an artistic sense. It needs to be readable in a functional sense. Those are different things, and the latter matters far more.

Typography and Layout

One font family, maximum two weights (regular and bold). Space Grotesk, Inter, or a clean sans-serif works well. Body text at minimum 14pt. Headlines at 28-36pt. Nothing smaller, ever. If you can't fit the content at those sizes, your slide has too much text — edit ruthlessly.

Dark text on a light background remains the gold standard for readability. Light text on dark backgrounds works for headlines only. Never mix multiple fonts. Never use all-caps for more than 3 words. The design should disappear — the investor should see your message, not your layout.

Related: Pitch Deck Fonts and Colors That Work (Coming soon — September 15, 2026)

Data Visualization

Every chart should pass the "grandma test" — your grandmother should be able to understand it in 5 seconds without explanation. Line charts for trends over time. Bar charts for comparisons. Simple tables for specific numbers. Pie charts only with 2-4 segments and clear labels.

Never use 3D charts, radar charts, or anything that requires a legend to decode. If your chart needs a footnote, the chart is wrong. Label your axes directly. Put the key number in bold at the top. The data should tell the story without the investor having to work for it.

Related: Pitch Deck Data Visualization Best Practices

Slide Count and Flow

10 slides for the main deck. 15-20 appendix slides for follow-up meetings. The appendix is where you put technical architecture, detailed financial projections, full customer testimonials, competitive deep-dives, team bios, and anything else that supports the narrative without belonging in the main flow.

When an investor asks a question during a meeting, having an appendix slide that directly answers it shows preparation and confidence. "Great question — I have a slide for that. Let me jump to the appendix." This is a power move.

Related: How Many Slides Should a Pitch Deck Have? (Coming soon — October 27, 2026)

Investor Psychology: What's Really Going On

Understanding what's happening in an investor's head during your pitch changes how you build every slide and how you deliver every answer.

Pattern Matching

Investors see 500-1,000 decks a year. They're pattern-matching constantly. If your deck looks like the last 10 they saw, it blends into statistical noise. Not because investors are unfair — because the human brain optimizes for efficiency and your deck is competing for attention against hundreds of others.

The solution isn't to make your deck weird or flashy. It's to be clearer, tighter, and more focused than the other 99 decks they saw this quarter. Every slide should have one message and one message only. The deck that communicates the most with the fewest words wins.

The FOMO Button

Social proof is the most powerful psychological lever in fundraising. Mentioning a lead investor, a notable advisor, or recognizable customers early in the deck activates FOMO in other investors. Use it strategically.

But don't ever fake it. Falsified traction or fake customer logos will be discovered in diligence and will kill your round permanently. Investors talk to each other. The fundraising community is smaller than you think, and reputation is everything.

Related: Pitch Deck Social Proof Strategies (Coming soon — November 20, 2026)

The Risk Checklist

Investors are subconsciously running through a risk checklist during your pitch: team risk (can these people execute?), market risk (is there a real market?), product risk (can they build it?), timing risk (is this the right moment?), competition risk (can someone else do it faster?), execution risk (can they actually deliver?), capital risk (will they run out of money?).

Every slide should address at least one of these risks. If a slide doesn't reduce perceived risk in the investor's mind, cut it. Every piece of content in your deck should serve the single purpose of removing an objection before it's raised.

Common Mistakes That Kill Decks

Avoid these and you're already ahead of 80% of the decks investors see.

The Curse of Knowledge

You've been living in your business for months or years. Everything about it seems obvious to you. It's not obvious to the investor, who is seeing your company for the first time in a 30-minute window between other meetings.

Get a friend who knows nothing about your space to read your deck cold. If they can't explain your business clearly afterward, rewrite until they can. The test isn't whether they remember the details — it's whether they can articulate the core thesis in one sentence.

Death by Detail

Technical founders love including architecture diagrams, feature lists, and engineering implementation details. Investors don't care about any of it at the pitch stage. They care about the problem, the market, the traction, and the team. Everything else is noise that distracts from the signal.

Saving details for the appendix isn't hiding them. It's prioritizing the investor's attention. The person who wants to know about your tech stack will ask — and you'll have a slide ready. The person who doesn't ask won't miss it.

Weak Opening

The first slide sets the tone for the entire meeting. If it's just your logo and a tagline, you've wasted the most valuable real estate in your deck. Start with a bold claim, a relatable problem story, or a surprising data point that makes the investor sit up.

Your opening slide should make the investor think "I need to know more about this." If it doesn't, your job just got harder.

Related: Common Pitch Deck Mistakes and How to Fix Them

Vanity Metrics

Total registered users means nothing. Monthly active users, paying users, retention rates, revenue — those mean something. Every metric in your deck should be something that a skeptical investor would accept as real signal. If you wouldn't want an investor to ask "how many of those are active?" about a metric, don't put it in the deck.

Ignoring the Competition Slide Standard

Everyone has competitors. Pretending you don't makes you look naive or dishonest. The most dangerous competitor is the one the investor already knows about. If you don't address them, the investor will wonder why you're ignoring the elephant in the room. Acknowledge the competitive landscape, show your differentiation honestly, and move on.

Related: Pitch Deck Dark Patterns That Repel Investors (Coming soon — September 27, 2026)

Beyond the Deck: The Full Pitching Ecosystem

Your deck is one piece of a larger system. Here's how the other pieces work.

The Pre-Meeting Deck

Send a 6-8 slide teaser deck before the meeting. Keep it tight — problem, solution, market, traction, team, ask. If an investor likes the teaser, they'll ask for the full deck in advance of the meeting or at the meeting itself. This gives you a second chance to make a first impression.

Related: Pre-Meeting vs. In-Person Pitch Decks (Coming soon — January 10, 2027)

The Pitch Email

Subject lines matter more than you think. "Seeking introduction — [Startup Name] — [One-liner]" is a common pattern that works because it's clear, direct, and respects the recipient's time. Attach a PDF of your teaser deck, not a link. Links get ignored or flagged as spam. PDFs get opened.

Related: Pitch Deck Email Subject Lines That Get Opened (Coming soon — October 15, 2026)

The Appendix Strategy

Your appendix should answer every question you've ever been asked in a pitch meeting. Every time an investor raises an objection or asks a clarifying question, that's a slide you need in your appendix. When an investor asks "what about X?" you say "great question — slide 24" and flip to it. That's confidence. That's preparation. And it signals that you've thought deeply about your business.

Related: The Pitch Deck Appendix Guide (Coming soon — August 16, 2026)

Demo Day vs. Investor Meeting

Demo day pitches are different from one-on-one investor meetings. Demo day is about energy, storytelling, and standing out in a lineup of 10-15 companies. Investor meetings are about substance, data, and answering hard questions. Don't use the same deck for both. Build two versions.

Related: Demo Day Pitch Deck vs. Fundraising Deck (Coming soon — October 9, 2026)

Tailoring by Stage and Sector

Your stage and sector determine what your deck needs to emphasize.

Pre-Seed (No Revenue)

Your deck needs to scream "this team will figure it out." With no revenue, traction substitutes include waitlist signups, customer interviews, letters of intent, advisor credibility, and domain expertise. The deck should be heavier on team and problem, lighter on business model and financial projections. Investors at this stage are betting on the jockey, not the horse.

Related: Pre-Seed Pitch Deck With No Revenue (Coming soon — August 10, 2026)

Seed Stage

You need revenue or strong user traction. Show MRR or active users with a growth curve, and show a clear path to Series A metrics within 12-18 months. The deck should demonstrate early product-market fit signal — repeat purchases, organic growth, or strong retention. At seed, you're proving that something is working; you don't need to prove everything.

Series A and Beyond

At Series A, investors expect proven unit economics, predictable growth, and a large addressable market. Your deck is less about conviction and more about evidence. Show cohort retention curves, not just averages. Show NRR above 100%. Show efficient unit economics. Show why you're the category winner, not just a participant.

Related: Seed vs. Series A Pitch Deck Differences (Coming soon — August 4, 2026)

SaaS

Focus on metrics: MRR, NRR, churn, CAC, LTV, magic number, burn multiple. Every slide should tie back to a metric that matters. SaaS investors have a specific mental model of what healthy looks like, and your deck needs to fit that model while showing why you're an outlier.

Related: SaaS Pitch Deck Examples That Raised (Coming soon — August 22, 2026)

Biotech / Hardware

Longer timelines, larger capital requirements, higher technical risk. Your deck needs to show milestone-based progress and specific de-risking events. Investors in these sectors care about regulatory path, IP moats, manufacturing partnerships, and clinical or engineering milestones. The timeline to exit is longer, so the story needs to be correspondingly more compelling.

Related: Biotech Pitch Deck Strategy (Coming soon — August 28, 2026), Hardware Pitch Deck Guide (Coming soon — January 2, 2027)

AI Startups (2026)

The AI market is saturated. Every investor has seen hundreds of "AI for X" pitches. Your deck needs to show defensible moats — proprietary data that no one else has, distribution advantage from an existing user base, or deep technical barriers that competitors can't replicate quickly. Saying "we use AI" in 2026 is like saying "we have a website" in 2000. It's table stakes, not differentiation.

Related: AI Startup Pitch Deck in 2026 (Coming soon — January 14, 2027)

Examples That Raised Real Money

The best way to learn pitch deck structure is to study decks that actually closed rounds. We've analyzed dozens of decks that raised from top-tier firms. The patterns are clear: clean design, one message per slide, narrative cohesion, and ruthless editing. Study patterns, not templates. The specific order of slides matters less than the narrative logic that connects them.

Related: Y Combinator Pitch Deck Template (Coming soon — November 14, 2026), Billion Dollar Pitch Deck Examples (Coming soon — October 21, 2026), Pitch Deck Templates That Raised Money

FAQ

How long should my pitch deck be?

10 slides for the main deck, plus 15-20 appendix slides. Never go over 12 slides in the main deck — if you have more, you haven't edited ruthlessly enough. A 15-slide deck is a 15-slide problem.

Should I send my deck before the meeting?

Send a teaser version (6-8 slides) before the first meeting. The full deck goes after the meeting, or when an investor specifically asks for it. Sending the full deck unsolicited reduces your control over the narrative.

What's the most important slide?

The problem slide. If you don't make the investor viscerally feel the problem, nothing else matters. Traction is a close second — it's the slide that turns your story into evidence. But the problem slide is where you win or lose attention.

Do I need a pitch deck designer?

You need a clean, readable deck. If you can design that yourself, great. If you can't, hire someone for a few hundred dollars. But don't spend $5,000 on design before you've validated the content and flow. Content-first, design-second, always.

How do I handle the competition slide?

Acknowledge your competitors honestly. Show a landscape or comparison matrix. The key is to demonstrate structural differentiation — something incumbents can't easily copy. Avoid claiming "we have no competition." Every investor knows that's either naive or false, and either way it's disqualifying.

Ready to build a deck that raises your round? Upload your pitch deck to Bullpen for a free AI-powered analysis across 7 evaluation categories — including investor psychology, market positioning, and narrative structure. Get actionable feedback before you send it to investors.

Get weekly pitch tips

One email a week. Actionable advice for founders.

Upload your deck. Get scored in 2 minutes. Free. Try now →