The Startup Fundraising Playbook: From Pre-Seed to Series A

A comprehensive guide to the startup fundraising lifecycle — when to raise, how much to raise, which instruments to use, how valuation works, and how to navigate term sheets.

Fundraising is not a milestone. It's a means to an end. The best founders raise money efficiently — asking for exactly what they need, at the right time, from the right investors — and then get back to building. The worst founders treat fundraising as a full-time job and end up with a lot of meetings and not enough money in the bank.

The fundraising landscape in 2026 is different than it was even three years ago. SAFE notes are the standard for pre-seed and seed. AI startups have compressed fundraising timelines. International investors are more active than ever. And the bar for Series A is the highest it's ever been — $2-3M ARR with 30%+ MoM growth and proven unit economics is the new baseline.

This guide walks the full lifecycle from pre-seed to Series A, covering strategy, mechanics, and psychology at each stage. It's written for founders who want to raise once and raise well.

When to Raise: Timing Your Fundraising

The single biggest mistake founders make is raising too early or too late. Raising too early means you give away equity before you have any leverage. Raising too late means you're negotiating from desperation. Both are avoidable.

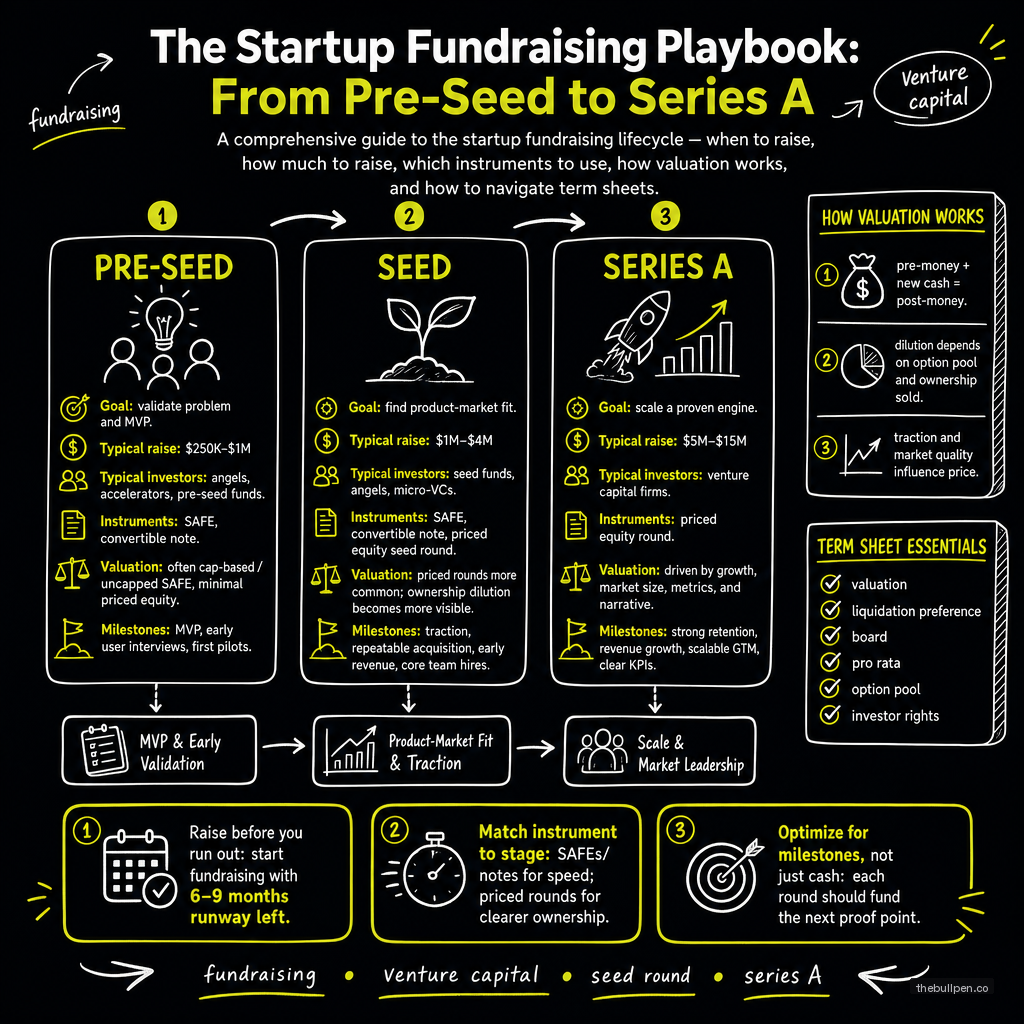

The Runway Rule

Start fundraising when you have 5-6 months of runway remaining. Fundraising always takes twice as long as you think — at least 3 months for a warm round, 4-6 months for a cold round. If you wait until you're at 3 months of runway, you're negotiating from weakness and investors will smell the desperation.

A 12-18 month post-funding runway is the target. Less than 12 months means you'll be back fundraising before you've made meaningful progress on your milestones. More than 18 months can breed complacency and reduce the urgency that drives early-stage execution. The sweet spot is right around 15-16 months.

Related: Efficient Fundraising Process: A Step-by-Step Guide (Coming soon — November 15, 2026), Fundraising While Operating Your Company (Coming soon — September 4, 2026)

The Momentum Window

Raise when you have a strong narrative. The best time is right after a notable milestone — a product launch, a key hire, a major customer win, a growth inflection that shows in the numbers. Fundraising into momentum compounds: investors see other investors interested, which makes them more interested. Fundraising from a flat position is a grind.

Think of fundraising as a wave: you want to catch it at the peak, not paddle for it when the water is still. The difference between raising when you're growing at 20% MoM vs. 15% MoM is the difference between a competitive round and a process.

Seasonal Considerations

Q1 (January-February) is slow because partners are returning from holidays, setting annual budgets, and digesting Q4 deal flow. Q4 (October-December) is slow because of holidays, budget exhaustion, and year-end portfolio reviews. Q2 (April-June) and early Q3 (July-September) are the sweet spots — partners are active, deal flow is steady, and there's enough time in the year to close before the holiday slowdown.

If you can time your raise for April through June, you'll have more attention from fewer competing deals. This is a tactical advantage that costs nothing but planning.

Fundraising Instruments: What to Use When

The instrument you choose shapes your cap table, your dilution trajectory, and your relationship with investors. Each has a time and place.

SAFE Notes (Standard in 2026)

SAFEs (Simple Agreement for Future Equity) remain the dominant pre-seed and seed instrument. They're simple, fast, and relatively cheap to issue — typically $5-15K in legal fees compared to $50-150K for a priced round. The key terms to negotiate are the valuation cap, the discount rate, and the most-favored-nation (MFN) clause.

Standard ranges in 2026: valuation caps from $5M-$15M for pre-seed, $10M-$30M for seed. Discount rates typically 15-25%. The MFN clause is more important than most founders realize — it ensures that if the startup issues a later SAFE with better terms, earlier investors can adopt those terms. Don't obsess over the valuation cap. Obsession signals inexperience and wastes negotiation capital on the wrong variable.

Related: SAFE Notes vs. Convertible Notes: Which Is Right for You?

Convertible Notes

Less common than SAFEs but still useful in certain situations — particularly for international investors who are more familiar with debt structures, or for investors who prefer the additional investor protections that notes provide. Convertible notes accrue interest (typically 2-8% per year) and have a maturity date (typically 18-24 months).

The maturity date is a ticking time bomb. If you haven't raised your next round by the maturity date, the note either converts at the valuation cap or becomes due (plus interest). Push for 24+ months and clean extension terms. A note that matures during a difficult fundraising market can cause serious problems.

Priced Equity Rounds

In a priced round, investors buy shares in your company at a fixed valuation with a set share price. It's more expensive in legal fees ($50K-$150K) but gives cleaner terms and establishes a clear valuation benchmark for future rounds. Priced rounds are standard for Series A and beyond, and increasingly common for larger seed rounds ($2M+).

The trade-off: priced rounds require more negotiation, more documentation, and more board governance. But they also provide more certainty and cleaner cap table management. For larger rounds, the clean structure is worth the extra cost.

Related: Priced Equity Rounds: When and Why

Venture Debt

Debt that sits alongside equity — not a replacement for it. Useful for extending runway between equity rounds without further dilution. Best suited for companies with recurring revenue, gross margins above 70%, and proven unit economics. Venture debt lenders charge interest (typically 10-15% APR) and often require warrants (small equity kickers, typically 5-15% of the loan amount).

Venture debt is not appropriate for pre-revenue companies. If you don't have revenue, you can't service debt, and the lender will require personal guarantees or other onerous terms that make it a bad deal.

Related: Venture Debt Guide: What Every Founder Should Know (Coming soon — August 17, 2026), Venture Debt Guide Part 2 (Coming soon — November 9, 2026)

How Much to Raise

The answer is always "enough to reach a clearly defined next milestone that increases your company's value." Not "as much as possible." Raising too much is almost as bad as raising too little.

The Milestone-Based Approach

Work backward from your next value inflection point. For pre-seed to seed, that's usually product-market fit signal or $1M ARR. For seed to Series A, it's typically $2-3M ARR with 30%+ MoM growth, >70% gross margin, and >100% NRR. For Series A to Series B, it's scaling the go-to-market engine and proving repeatability.

Calculate exactly how much you need to reach that milestone, add 30% for buffer and variance, and that's your round size. Anything beyond that is dilution without corresponding value creation.

Related: Seed Round Strategy 2026: How Much and When

The Dilution Math

Target 15-25% dilution per round. If you're giving up more than 25% in a single round, something is wrong — either you're raising too much, your valuation is too low, or you haven't shown enough traction for the stage you're raising at.

Run a dilution model across multiple rounds. A founder who starts with 60% ownership, raises a seed round at 20% dilution (now owns 48%), a Series A at 20% (38.4%), a Series B at 15% (32.6%), and a Series C at 10% (29.4%) — that's a healthy trajectory. A founder who raises a seed round at 30% dilution is already behind.

Related: Fundraising Math: Dilution and Ownership (Coming soon — January 19, 2027), Financial Model for Fundraising (Coming soon — October 28, 2026)

The Oversubscription Trap

Raising more than you need sounds like a good problem to have. It's often not. Too much capital can mask operational inefficiency, create false product-market fit signals (money buys growth that isn't organic), and lead to overspending on headcount and marketing before the unit economics are proven.

There's a reason most high-profile startup blow-ups happen after highly visible, overcapitalized rounds. When money is cheap, discipline is expensive. Stay lean until you've proven repeatability.

Building Your Investor Target List

You need 50-100 target investors for a successful raise. Most will say no. That's normal. The math of fundraising is a volume game with a conversion rate that's lower than you'd hope.

Tier 1: Perfect Fit

10-15 investors who match your stage, sector, check size, geography, and investment thesis. These get full personalized treatment — warm introductions, customized deck versions, tailored narrative. Research each partner's portfolio and recent investments obsessively. Know what they've said publicly about your space.

The goal with Tier 1 is not just to get a check. It's to find your lead investor — the person who will anchor your round, set the terms, and bring other investors in. A strong lead is worth their weight in gold.

Tier 2: Good Fit

20-30 investors who mostly match but have one dimension off — maybe they're a stage late, or they don't usually invest in your geography, or their check size is smaller than ideal. Warm introductions still preferred, but thoughtful cold emails with a compelling subject line and a clear reason for reaching out can work.

Tier 3: Shotgun

30-50 investors in your broader ecosystem. These get the same deck and a standard email template with minimal personalization. The conversion rate will be 1-3%, but volume compensates. Never skip Tier 3 — sometimes the best investors come from unexpected places.

Related: How to Find the Right VC Firm for Your Startup (Coming soon — October 4, 2026), Warm Introduction Strategy for Fundraising

Investor Targeting Best Practices

Filter by: stage focus (check the fund size — $50M funds can't write $5M checks), sector expertise, check size range, board seats available, portfolio density (too many investments in your space means less attention for you), follow-on fund capacity, and reputation with portfolio companies.

Tools like PitchBook, Crunchbase, and Notion trackers help. But the simplest system — a spreadsheet with 100 rows, 10 columns, and a status tracker — beats no system. The best CRM for fundraising is the one you actually use.

Term Sheets: What to Actually Read

Term sheets are confusing by design. Here's what matters and what's noise.

Economic Terms

- Valuation / Price: The number everyone obsesses over. Important, but not the only thing that matters. A high valuation with bad governance terms is worse than a fair valuation with clean terms.

- Liquidation Preference: How the pie is divided in an exit. 1x non-participating is standard. Anything above 2x or participating preferred (where the investor gets their money back and shares in the remaining proceeds) is bad for founders. Avoid at all costs.

- Pro rata rights: The investor's right to participate in future rounds to maintain their ownership percentage. Standard for lead investors. Non-standard: forcing pro rata on all future rounds with a minimum investment amount.

- Anti-dilution provisions: Full-ratchet anti-dilution is terrible for founders — it means if you raise a down round, earlier investors get shares to make up the difference, diluting you massively. Weighted average anti-dilution is standard and fair.

Governance Terms

- Board composition: 2:1 founder-to-investor ratio is ideal. 3 seats total for early rounds — 2 founders, 1 investor. Adding a third founder seat is fine. Giving investors control of the board early is not.

- Protective provisions: What needs investor approval beyond their board seat. Standard list is fine (changing authorized shares, selling the company, taking on significant debt). Broad list that lets a minority investor veto operational decisions is not.

- Information rights: Standard monthly financials, quarterly board decks, annual budgets. This is table stakes.

- Drag-along rights: Allows majority shareholders to force a sale. Standard and usually fair — it prevents a minority shareholder from blocking an exit that benefits everyone else.

Related: How to Read a Term Sheet (Coming soon — September 16, 2026), Term Sheets Decoded: A Clause-by-Clause Guide

Red Flags to Watch

Participating preferred with uncapped participation. Full-ratchet anti-dilution. Personal guarantees on any terms. No-shop clauses longer than 45 days (you need time to run your process). Excessive protective provisions that let a minority blockholder control the company. Any term that treats founders differently from each other.

Valuation: How Early-Stage Pricing Works

Valuation at the early stage is more art than science, but there's logic behind the ranges.

Pre-Seed Valuation

Typically $4M-$10M post-money. The range is driven by team quality (previous exits, domain expertise), market size, and early traction signals (waitlist, prototype, LOIs). No revenue with a great team in a large market? $4M-$6M. Revenue with 10%+ MoM growth? Higher.

Seed Valuation

$10M-$30M post-money. Driven by MRR ($10K-$50K target range), growth rate (15%+ MoM), and competitive dynamics (multiple term sheets drive the valuation up). Companies at the upper end of this range have strong team-market fit, clean unit economics, and accelerating growth.

Series A Valuation

$30M-$80M+ post-money. The bar: $2-3M ARR, 30%+ MoM growth, >70% gross margin, >100% NRR, proven repeatable GTM. At this stage, valuation is driven by ARR multiples (typically 15-30x ARR for high-growth SaaS).

Related: Valuation Methods for Early-Stage Startups

What Actually Moves the Needle

Growth rate is the single biggest valuation driver at every stage. Higher growth = higher multiple = higher valuation. Everything else — team quality, market size, product sophistication — sets the floor. Growth rate sets the ceiling. A company growing at 30% MoM will always be valued higher than a company growing at 10% MoM, even if the slower-growing company has better margins.

The Fundraising Process, Step by Step

Phase 1: Preparation (4-6 weeks)

Build your investor target list. Prepare your data room with financial projections, cap table, key documents. Refine your deck until it's tight. Practice your pitch 20+ times with different audiences. Secure 2-3 warm introductions to start the process.

Related: Fundraising Data Room Checklist (Coming soon — September 22, 2026), Pre-Seed Fundraising Playbook

Phase 2: Initial Outreach (2-3 weeks)

Start with Tier 1 targets. Send personalized emails referencing specific reasons for reaching out. Schedule initial calls. The goal is 10-15 first meetings in the first 2 weeks. Don't start with Tier 3 — you want to build momentum from strong leads.

Phase 3: First Meetings (3-4 weeks)

30-minute video calls or in-person meetings. Walk through the deck. Listen more than you pitch. The best questions come from genuine, engaged listening. After each meeting, send a thoughtful follow-up within 24 hours that references something specific from the conversation.

Phase 4: Follow-ups and DD (3-6 weeks)

Interested investors will ask for follow-up meetings, customer references, data room access, and partner meetings. The duration of this phase depends on how hot your round is. Hot rounds take 2-3 weeks. Cold rounds take 4-8 weeks. Use the time to build traction.

Phase 5: Close (2-3 weeks)

Once you have a committed lead, set a 2-3 week deadline to close the round. This creates momentum and FOMO. Investors who drag their feet get left behind. A tight close signals confidence and deal discipline.

Managing Investor Relationships

Fundraising doesn't end when the money hits the bank. It's the beginning of a long-term relationship.

The Investor Update

Send monthly or quarterly updates. Structure: highlights, lowlights, metrics, asks (what you need from them). The best investor updates are honest, concise, and specific. Early investors who receive good updates become your best champions in future rounds.

Related: Investor Update Email Guide (Coming soon — January 3, 2027), Managing Investor Relationships

Strategic vs. Financial Investors

Strategic investors (corporate VCs, industry partners) bring more than money — distribution channels, credibility, potential partnerships. But their incentives don't always align with yours (they may push you toward their parent company's priorities). Financial investors are simpler: they want returns. Both have their place on a cap table.

Related: Strategic vs. Financial Investors: What's the Difference? (Coming soon — August 11, 2026), Strategic vs. Financial Investors: Deep Dive (Coming soon — October 16, 2026)

FAQ

How long does a typical fundraise take?

3-6 months from start to money in the bank. Warm rounds (existing relationships, warm intros, strong traction) can close in 4-8 weeks. Cold rounds (no existing relationships, weaker traction) take 4-6 months.

Should I use a fundraising advisor or consultant?

Advisors can help with introductions and strategic advice, but be wary of anyone who promises to "raise your round for you." The best person to pitch your company is you. Advisors who charge retainers without delivery milestones are a red flag.

What's the most common reason seed rounds fail?

Lack of traction. Founders who try to raise with no customers, no revenue, and no serious user engagement data get told "come back when you have more signal." The second most common reason: misaligned valuation expectations between founder and market.

Do I need a lead investor for my seed round?

It helps enormously. A lead sets the terms, anchors the valuation, and signals quality to other investors. Without a lead, you're piecing together smaller checks, which is slower, more uncertain, and less efficient.

Can I raise internationally?

Yes, and it's becoming more common. US investors still write the largest checks, but European, Asian, and Middle Eastern VCs are increasingly active at the seed stage. Different regions have different norms, legal frameworks, and check sizes.

Related: International Fundraising: US (Coming soon — August 23, 2026), International Fundraising: EU (Coming soon — November 27, 2026)

Ready to prepare for your next round? Upload your pitch deck or financial model to Bullpen for a free AI-powered evaluation. Get objective feedback on your investor readiness before you start sending warm intros.

Get weekly pitch tips

One email a week. Actionable advice for founders.

See how investors will grade your pitch. Try now →