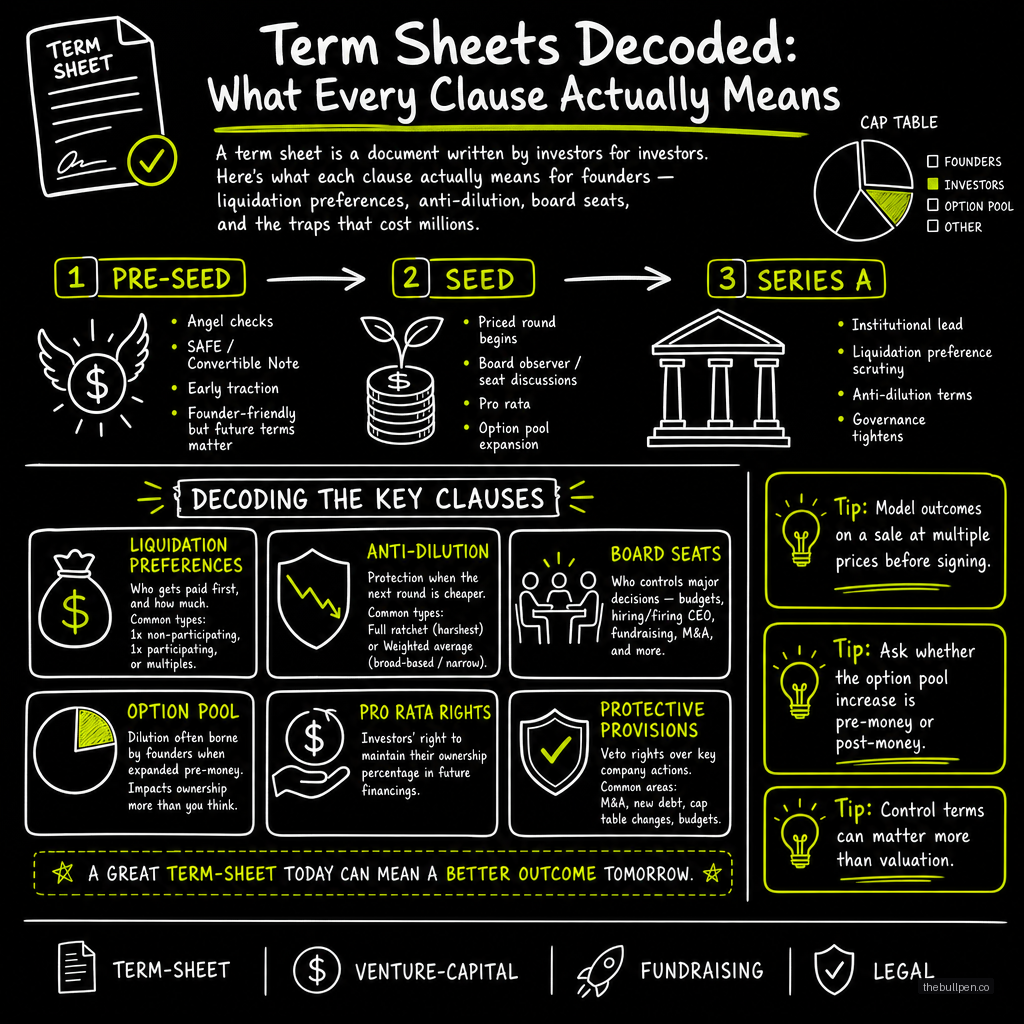

Term Sheets Decoded: What Every Clause Actually Means

A term sheet is a document written by investors for investors. Here's what each clause actually means for founders — liquidation preferences, anti-dilution, board seats, and the traps that cost millions.

A term sheet is not a negotiation between equals. It's a document drafted by the investor's lawyer, reviewed by the investor's partners, and presented to you — the founder who has never seen one before, who is under time pressure, and who is terrified of losing the round.

The asymmetry is built into the structure. The investor has seen 50 term sheets. You're seeing your first. They know which clauses are standard and which are aggressive. They know which terms they'll fight for and which they'll concede immediately. You don't know any of this — unless you've done the homework in advance.

This guide covers the clauses that actually matter. Not the legal boilerplate, not the standard language that every deal uses. The three or four terms that determine whether you keep control of your company and whether you get paid when it sells.

Related: The Startup Fundraising Playbook: From Pre-Seed to Series A

Liquidation Preference: The Most Important Clause

The liquidation preference determines who gets paid first when the company exits. This one clause can shift millions of dollars from founders to investors in a moderate exit.

A 1x non-participating preference — the standard for roughly 70% of Series A rounds — means the investor gets their investment back before common shareholders see anything, but then they stop. They make their one times return and the remaining proceeds are split among all shareholders according to ownership.

A 1x participating preference — found in about 25% of Series A rounds — means the investor gets their investment back AND then shares in the remaining proceeds. In a $50 million exit with $40 million in total investment, the difference between participating and non-participating can be millions of dollars.

| Liquidation Preference | Founder Impact | Example ($50M Exit, $10M Raised) |

|---|---|---|

| 1x non-participating | Fair — standard | Investors get $10M, founders split $40M proportionally |

| 1x participating | Aggressive | Investors get $10M + |

| 2x participating | Toxic | Investors get $20M + |

The difference between participating and non-participating matters most in the range between 1x and 3x return on investment. Above 3x, the economics converge because converting to common is usually better for the investor anyway. In the 1x to 3x range, participating preference can reduce founder proceeds by 30-50%.

Fight for non-participating. If the investor insists on participating, limit it with a cap — 2x max participation — so the preference stops after a reasonable return.

Anti-Dilution: Protection in a Down Round

Anti-dilution provisions protect investors if the company raises a future round at a lower valuation. Two types exist, and the difference is extreme.

Weighted average anti-dilution — used in over 95% of Series A rounds — adjusts the investor's conversion price based on the size and price of the down round. A down round at 20% below the Series A price triggers a modest adjustment. The formula is designed to be fair to both sides.

Full ratchet anti-dilution — rare but destructive — resets the investor's price to the lowest price ever paid by any subsequent investor. If you raise a bridge round at half your Series A valuation, every investor with full ratchet gets to convert their shares at the new lower price. The result is catastrophic dilution for founders and employees.

Never agree to full ratchet. Most investors won't ask for it at Series A. If they do, push for standard weighted average.

Board Composition: Who Controls What

The board of directors makes the most important decisions a startup faces: hiring and firing the CEO, raising additional capital, selling the company, and issuing equity to employees. Board composition determines who controls these decisions.

A typical Series A board has five seats: two founders, two investors, and one independent or mutually agreed member. This structure means no single party has unilateral control — the investors can't outvote the founders together, and the founders can't outvote the investors.

The trap founders fall into is agreeing to a board where investors hold the majority. If the investor has three seats and founders have two, the investor controls the board. They can fire the CEO (you), force a sale you don't want, or block strategic decisions.

If you can't avoid an investor-majority board, negotiate a sunset provision: after five years, or after certain performance milestones are met, the board flips to founder majority. This gives you an off-ramp from investor control without fighting the structure at signing.

| Board Structure | Who Controls | Risk Level |

|---|---|---|

| 2 founders + 1 investor + 1 independent | No one — balanced | Minimal |

| 2 founders + 1 investor | Founders | Low — standard for seed |

| 2 founders + 2 investors + 1 independent | Depends on independent | Moderate — negotiate carefully |

| 2 founders + 3 investors | Investors | High — fight this |

Related: SAFE Notes vs Convertible Notes: Which One Should You Use?

The Option Pool Trap

The option pool — shares reserved for future employees — is one of the most misunderstood line items in a term sheet. The pool is typically 10-20% of the company, and the key question is whether it's included in the pre-money valuation or added on top of it.

If the investor offers a $10M pre-money valuation with a 20% option pool already included, your effective valuation is $8M. The pool comes out of the founders' side because it's built into the pre-money. If the option pool is added on top of the pre-money, the dilution is shared between founders and investors.

Founders who focus only on the headline pre-money number and ignore the option pool allocation often end up with less ownership than they expected. Always negotiate the pool size and allocation as part of the valuation discussion.

Pro-Rata Rights and Information Rights

Pro-rata rights allow investors to participate in future rounds to maintain their ownership percentage. This is standard for lead investors and generally founder-friendly — it ensures your existing investors can continue to support you.

Information rights require you to provide regular financial updates — typically monthly or quarterly. Standard, but the scope matters. Some term sheets require audited financials once the company reaches a certain size. Make sure the requirements are manageable for your current stage.

The Negotiation Itself

Term sheet negotiations follow a predictable pattern. The investor leads with an aggressive first draft. Founders push back on 3-4 key terms. The negotiation focuses on those terms while the standard boilerplate passes through unchanged.

The most effective negotiation strategy is to have a second investor. Competition transforms your leverage. If the investor knows you have another term sheet, they'll improve their terms without being asked. If a clause can't be improved, knowing you have an alternative gives you the confidence to walk away.

The best time to learn term sheet mechanics is before you need them. When the document arrives and the clock is ticking, you don't want to be Googling "what is participating preferred" while a partner waits for your response.

Published on the Bullpen Blog. New articles every day at 9 AM UTC.

Get weekly pitch tips

One email a week. Actionable advice for founders.

See how investors will grade your pitch. Try now →