Series A Preparation: What VCs Actually Look For

The Series A bar has never been higher. Here's exactly what VCs look for in 2026 — ARR thresholds, growth rates, unit economics, and how to know if you're ready.

The difference between a seed round and a Series A is not the amount of money. It's the amount of evidence.

At seed, you're selling potential. Your idea, your team, your market, your early traction — all of it points to what could be. At Series A, potential is no longer enough. The investor needs to see that the machine is working. You need revenue. You need retention. You need a repeatable path to $100M ARR, backed by data that makes it plausible.

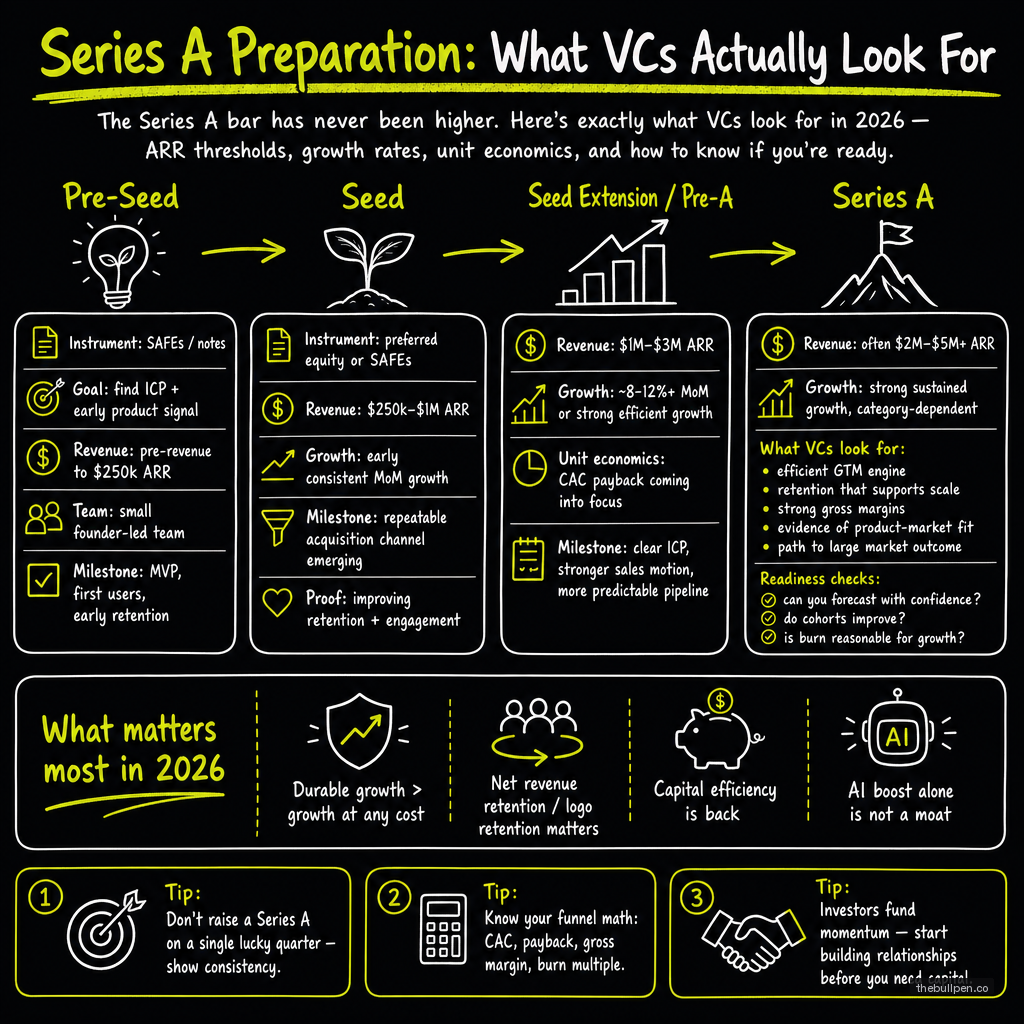

In 2020, the bar for Series A was roughly $1M ARR with strong growth. In 2026, that bar has effectively doubled. The median Series A company today has $2M to $3M ARR at close, with growth rates that would have been considered exceptional five years ago. This shift has created the "Series A crunch" — a growing gap between the number of seed-funded startups and the number that graduate to Series A.

The data is sobering. According to Carta's 2024 cohort analysis, only 25 to 30 percent of seed-stage companies raise a Series A. That's down from roughly 40 percent in 2021. The bar moved, and it moved fast.

Related: Seed Round Strategy: Raising $1M-$5M in 2026

The Scorecard: What VCs Evaluate

Series A investors evaluate companies across five dimensions, and you need to be strong in at least four of them to get a term sheet.

Revenue and growth is the heaviest-weighted factor. You need $2M to $3M ARR for a competitive Series A in 2026, with month-over-month growth of 10 to 15 percent. Companies growing below 10% MoM at $2M ARR are usually told to come back when they're growing faster or have more revenue. The Rule of 40 — growth rate plus profit margin — isn't expected at Series A, but investors notice it. The growth rate expectations: 3x year-over-year is strong. 4x is exceptional. 2x is borderline for most firms.

Retention and unit economics is where most companies get filtered out. Net Revenue Retention above 100% is table stakes. Above 120% is considered elite. Gross Revenue Retention should be 80% or higher — if you're losing more than 20% of your revenue annually to churn, your growth treadmill is working against you. Gross margins below 70% raise questions about whether you have a product business or a services business. LTV:CAC ratio below 3x means you're buying revenue, and the investor will model what happens when you stop buying.

Market size and position is about narrative as much as data. You need a credible path to $100M ARR, backed by either a large TAM or a clear niche with expansion potential. Investors want to believe that your current growth rate can sustain for several more years without hitting a ceiling.

Team and founder-market fit is about whether you're the right person to build this company. At Series A, the question shifts from "can you build the product" to "can you build the organization." Investors want to see that you've hired well, that your leadership team is scaling, and that you can attract talent competitive with larger companies.

Competitive position is about defensibility. Why won't a larger company copy you? What's your moat? For AI startups especially, this question is getting harder — many Series A investors now expect proprietary data, network effects, or deep technical moats as a precondition.

Related: Valuation Methods for Early-Stage Startups

The Series A Process

Series A is a different process from seed. At seed, you're pitching 50 to 100 investors and hoping for a few yeses. At Series A, you should be targeting 15 to 20 firms seriously, with a handful of strong candidates leading the process.

The timeline is longer. From first meeting to term sheet, expect 3 to 6 months. The first month is intros and initial meetings. The second month is deeper diligence — customer calls, product demos, financial modeling. The third month is partnership meetings, where the investor presents your company to their full partnership for a vote.

You should start the process when you have 9 to 12 months of runway remaining. Starting earlier gives you leverage — if a round takes 5 months, you want to close with 4 to 7 months of runway left, not zero. Founders who start fundraising when they have 3 months of runway left negotiate from a position of desperation, and it shows.

The firms that write Series A checks are largely the same names: a16z, Accel, Benchmark, Sequoia, Lightspeed, General Catalyst, Index, Felicis, Bessemer, CRV, Khosla, Founders Fund, and a long tail of strong second-tier funds. But getting a meeting requires a warm introduction from a trusted source. Cold emails at the Series A level have essentially zero conversion. Build relationships with these firms six to twelve months before you plan to raise.

The Readiness Checklist

Before you start meeting Series A investors, run through this checklist:

Product-market fit is demonstrated, not claimed. You have cohort retention data showing that customers who signed up six months ago are still active at the same rate as customers who signed up last month. Churn isn't zero, but it's stable and trending down.

You have a repeatable sales motion. You can point to a specific ICP, a specific channel, and a specific sales cycle that produced your last 20 customers. If each of those 20 came from a different channel with a different deal structure, you don't have a repeatable motion yet.

Your financial model is defensible. You can explain your revenue growth in terms of headcount, channel capacity, and market penetration — not just "we'll grow at 15% MoM because that's what we've been doing." A model that assumes linear scaling of current growth without accounting for market saturation or competition is a red flag.

Your unit economics are improving, not deteriorating. CAC should be flat or declining as your brand and content compound. LTV should be stable or increasing as you improve retention. If your unit economics are getting worse as you scale, the investor will assume they'll continue getting worse.

You have a credible plan for the capital. Series A investors want to know exactly how the $8M to $15M they're investing will get you to the next milestone. "We'll hire more engineers and grow" is not a plan. "We'll hire three sales reps to test our outbound motion in the enterprise segment, then based on those results, expand to two additional verticals in months 9 through 12" is a plan.

You are ready for the scrutiny. Series A diligence is intense. Investors will call your customers, your former employees, your competitors. They will model your financials from scratch. They will ask for cohort data, cap table details, and hiring plans. If any of these areas has a problem, find it and fix it before you start the process. The investor will find it eventually. Better to know about it first.

The Hard Truth

More startups will die in the gap between seed and Series A than at any other stage. The companies that make it through are not always the ones with the best products or the strongest teams. They are the ones that understand the math of Series A and build their companies to meet it — not because they're optimizing for investors, but because the same metrics that investors demand are the metrics that indicate a healthy, scalable business.

If your business doesn't meet the thresholds above, don't try to raise Series A early. You'll waste six months of runway on a process that ends in rejection, and you'll be worse off than when you started. Instead, focus on getting the metrics right. A later Series A with better numbers is worth more than an early one with weak fundamentals.

Data references: Carta's 2024 State of Private Markets (seed-to-A conversion rates, ARR thresholds), PitchBook/NVCA Venture Monitor Q4 2024 (median Series A size and valuations, growth benchmarks), Cooley GO Annual Report 2024 (metric thresholds by stage), YC Startup School (Series A process framework), SaaStr (Jason Lemkin — Series A readiness, Rule of 40, NRR benchmarks).

Ready to see where you stand? Upload your deck or financials to Bullpen for a free AI-powered evaluation across 7 investor categories — including revenue quality, unit economics, growth trajectory, and fundraising readiness.

Get weekly pitch tips

One email a week. Actionable advice for founders.

See how investors will grade your pitch. Try now →