Valuation Methods for Early-Stage Startups

How investors actually value early-stage companies — the VC method, scorecard, Berkus, and comps. And why the number matters less than you think.

Founders spend way too much time worrying about valuation. They obsess over whether their cap should be $8M or $10M. They stress about the difference between pre-money and post-money. They compare themselves to competitors and feel undervalued if the number is lower.

All of this misses the point. Early-stage valuation is not a science. It's a negotiation where the range of reasonable outcomes is wide enough that the exact number barely matters relative to the other terms on the table.

Here's what I've learned from watching dozens of rounds close: the valuation is the least interesting thing about a deal. Who the investor is, what they bring beyond money, and how much you raised are all more important. A $10M cap with the wrong investor is worse than an $8M cap with the right one.

Related: The Startup Fundraising Playbook: From Pre-Seed to Series A

How Investors Actually Think About Valuation

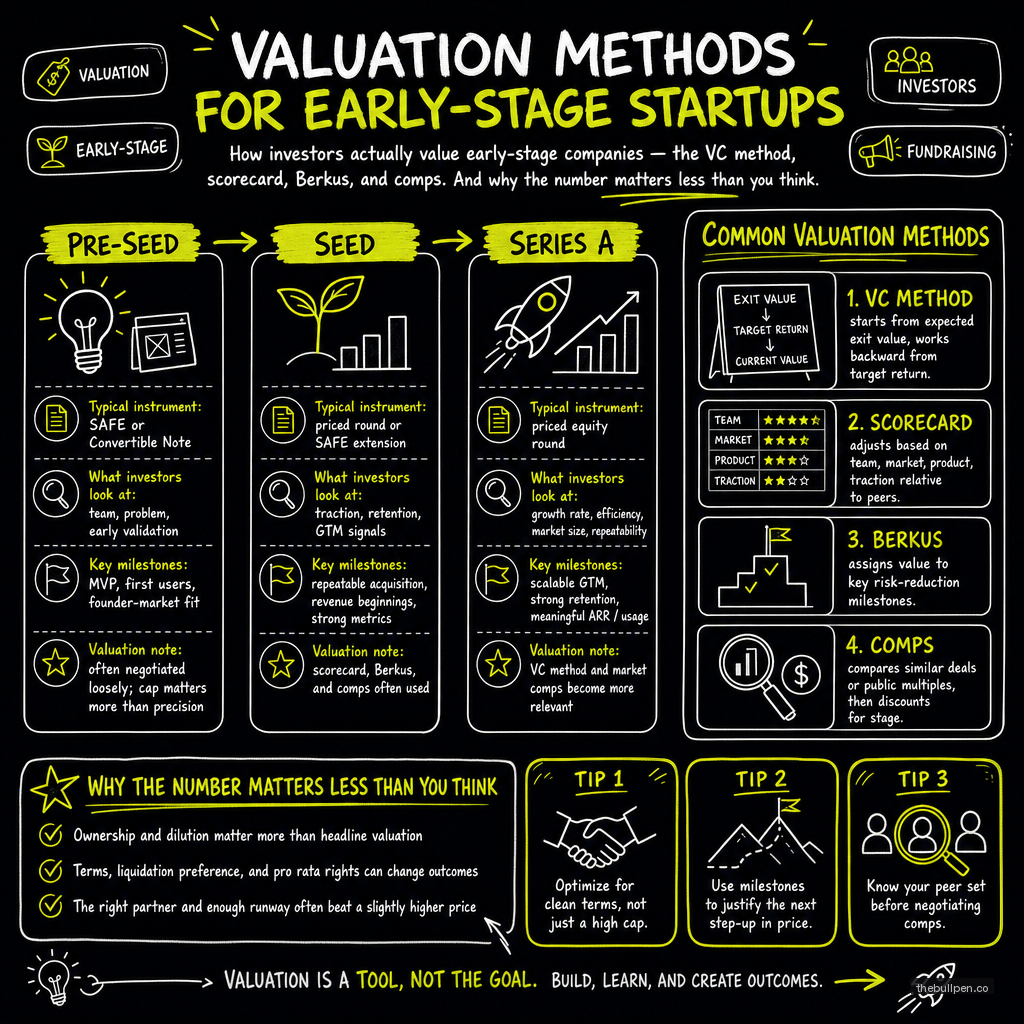

Investors at the pre-seed and seed stage don't use discounted cash flow models or comparable company analysis. There isn't enough data for that. Instead, they use a set of heuristics that triangulate on a reasonable number.

The most common framework is the VC method. It works backwards from the expected exit value. If the investor believes your company could be worth $100M in five years, and they want a 10x return on their investment, they need to own 10% of the company at exit. If they're investing $1M, that implies a post-money valuation of $10M, minus dilution from future rounds, adjusted down to maybe $7M or $8M post-money for the current round.

The math is crude but internally consistent. The output is a range, not a single number. Most investors arrive at a target ownership percentage and work backward from there.

The second framework is the scorecard method. The investor benchmarks your company against similar startups at your stage and adjusts for factors like team strength, market size, product stage, and competitive position. Each factor gets a weight, and the weighted average produces a valuation relative to the peer group.

The third framework is the Berkus method, which assigns a dollar value to five key risks: sound idea (up to $500K), prototype (up to $500K), quality management team (up to $500K), strategic relationships (up to $500K), and product rollout or sales (up to $500K). The maximum is $2.5M pre-money, which makes this method most relevant for very early pre-seed rounds.

| Method | Best For | Key Inputs |

|---|---|---|

| VC Method | Seed and Series A | Exit size, target return, dilution, timeline |

| Scorecard | Pre-seed to seed | Peer group benchmarks, weighted factor adjustments |

| Berkus | Idea-stage pre-seed | Five risk categories, max $500K each |

| Comparable transactions | Any stage | Recent similar rounds in your space |

What Actually Drives Your Valuation

In practice, four things determine your pre-seed or seed valuation more than any formal method.

Traction is the strongest signal. Revenue is the best traction. Users are second best. Anything that proves demand — waitlist signups, letters of intent, design partner commitments — counts. A startup with $10K MRR will almost always command a higher valuation than one with zero revenue but a "better idea."

Team quality is the second strongest signal. An experienced founder with a previous exit can raise at a 2x premium over a first-time founder with the same traction. A team with relevant domain expertise commands a higher valuation than a team that's learning the space. Investors are betting on the jockey, not the horse.

Market conditions set the ceiling. In a hot market (AI in 2024-2026, SaaS in 2021), valuations inflate across the board. In a cold market, they compress. The same company raising in different market conditions can see a 2x difference in valuation.

Investor demand determines where you land within the range. A competitive round with multiple term sheets drives valuation up. A single interested investor negotiating alone drives it down. The best way to improve your valuation is to create competition for the round.

The Cap Table Math

The most important valuation concept that founders overlook is the difference between pre-money and post-money, and how dilution compounds across rounds.

Pre-money valuation is the value of the company before the investment. Post-money is pre-money plus the investment amount. If you raise $2M on an $8M pre-money, your post-money is $10M, and the investor owns 20%.

That 20% is your dilution for this round. If you raise a Series A later at a $40M post-money, your existing investors get diluted again. After a typical seed and Series A, a founder who started with 100% ownership might own 40 to 50% of the company, depending on option pools and how much was raised.

The key insight: early-stage valuation matters less than the percentage you give up and the amount you raise. A $10M cap on a $2M raise gives away 20% of your company. An $8M cap on a $1.5M raise gives away 18.75%. The difference in dilution is trivial. The difference in runway — $500K — could be the difference between reaching product-market fit and running out of money.

Related: Cap Table Management: A Founder's Guide to Ownership Math

What Not to Do

Don't anchor on an unreasonable number. Founders who come in with a valuation that's 3x above market signal inexperience. Investors will either pass or grind you down to a fair number, and the process will take twice as long.

Don't lie about competing term sheets. Stretch the truth about competition and investors will find out. The venture community is smaller than you think, and partners talk to each other.

Don't optimize for valuation at the expense of everything else. The quality of your investor, the network they bring, the support they provide — all of these matter more than whether your cap was $8M or $10M. A lower valuation with a better investor is a better outcome than the reverse.

The round that matters most is not the one with the highest valuation. It's the one that sets you up to raise the next round. Everything else is theater.

Data references: Bill Payne's Scorecard Valuation Method, Dave Berkus' Berkus Method, VC Method (Sahlman/Howard), Carta's 2024 State of Private Markets (median SAFE caps $8M, ranges by sector), PitchBook Q1 2025 preliminary data.

Ready to see how investors would value your startup? Upload your pitch to Bullpen for a free AI-powered assessment across 7 investor categories.

Get weekly pitch tips

One email a week. Actionable advice for founders.

See how investors will grade your pitch. Try now →