The Pre-Seed Fundraising Playbook: From Zero to $1M

Everything first-time founders need to know about raising a pre-seed round in 2026 — check sizes, valuation caps, investors at this stage, what milestones to hit, and how the landscape has changed since 2020. Backed by real data from Carta, PitchBook, and Y Combinator.

Every first-time founder I meet wants the same thing: raise as much as humanly possible at the highest valuation cap they can negotiate, ideally from the most prestigious investor they can land.

That instinct is wrong on all three counts.

The difference between founders who raise again and founders who don't isn't the size of their pre-seed round or the name on their SAFE. It's understanding what pre-seed money is actually for: buying enough time to generate the signal that convinces someone to write a much bigger check later. Everything else is theater.

The Numbers Have Changed

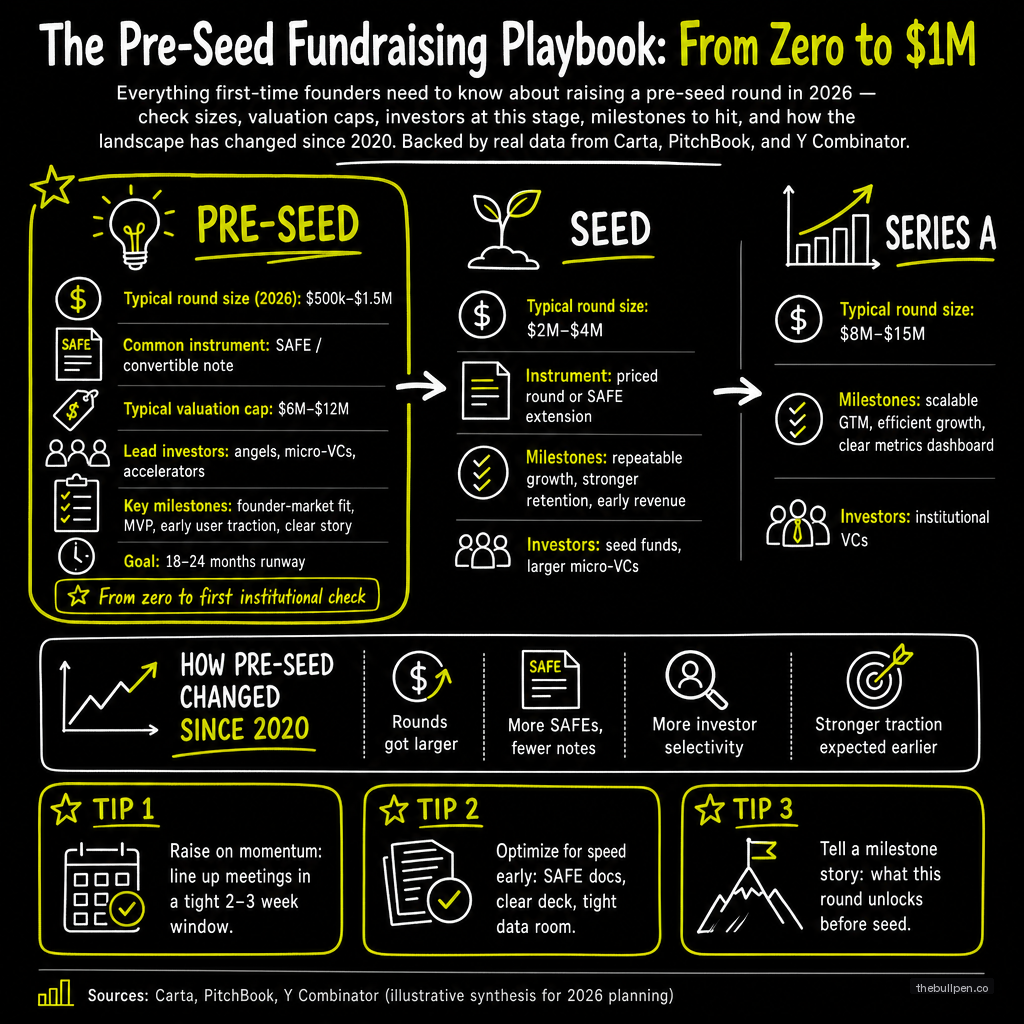

If you were raising five years ago, pre-seed meant a $500K round on a $5M cap from a few angel investors who you met through your college roommate. Those rounds still exist, but they're not the market anymore.

In 2026, the median pre-seed round sits between $1.5M and $2.0M, according to Carta's 2024 State of Private Markets and preliminary PitchBook Q1 2025 data. Valuation caps have moved in lockstep — the median SAFE cap is now $8M, with the top quartile landing at $12M and AI startups routinely clearing $15M. That's roughly double where things stood in 2020 across every dimension.

The instrument has standardized too. Almost everyone uses Y Combinator's post-money SAFE now. The uncapped SAFE with a discount — the default for most pre-seed rounds in 2020 — has all but disappeared. The market settled on a simpler, cleaner structure, and there's no reason to fight it.

Related: SAFE Notes vs Convertible Notes: Which Should You Use?

Who Actually Writes These Checks

The investor landscape at pre-seed looks nothing like it did five years ago. Angels used to dominate. Today, micro-VCs lead the vast majority of rounds, and rolling funds account for roughly 15–20% of pre-seed checks — particularly for founders outside the traditional startup hubs.

Neo, Precursor Ventures, Hustle Fund, Village Global, Afore Capital — these are the names you see leading pre-seed rounds in 2026, according to Carta's deal-count data. They write $500K to $2M per round. They've raised dedicated funds for exactly this stage, which means they need to deploy capital. If you fit their thesis, they're actively looking for you.

Rolling funds on AngelList filled the gap that individual angels left behind. They write smaller checks — $25K to $100K — but they're more accessible, especially if you're raising from outside San Francisco. Austin, Miami, Denver, London, Berlin — the geography of pre-seed has flattened.

The scout programs at Sequoia and a16z are worth noting too. They write pre-seed checks under the radar, often $500K to $1M, with less process than a full partnership vote. If you can get on a scout's radar, it's one of the cleanest paths to a top-tier name on your cap table without the top-tier diligence process.

What a Pre-Seed SAFE Actually Means

The number that founders obsess over — the valuation cap — matters less than you think. A $2M difference in cap on a $1.5M raise changes your dilution by roughly 3%. That's not nothing, but it's less important than who ends up on your cap table, how much you raised in total, and whether you left yourself enough room to raise again.

Here's what the market actually looks like right now. The 25th percentile pre-seed cap is around $5M. The median lands at $8M. The 75th clears $12M. Solo founders tend to land below the median — having a co-founder typically adds $1M to $2M to your cap, because investors price team risk directly. AI startups routinely raise at $12M to $15M caps, partly justified by compute costs and partly a market bubble that may or may not hold.

The terms that matter more than the cap: the discount rate (typically 15–25%), and the MFN clause — most-favored-nation, which means if you issue a later SAFE with better terms, earlier investors can adopt them. The MFN is standard. Don't negotiate it. Focus your energy on who's leading the round and what you're going to do with the money.

Related: Valuation Methods for Early-Stage Startups

What You Actually Need

The most common mistake first-time founders make is starting the process too early. They approach investors with a landing page and a dream, and then wonder why the meetings don't convert.

You need four things before you send your first email.

A working product. Not a Figma mockup, not a notion doc, not a landing page with a waitlist. A real MVP that a real user can interact with. For AI startups, a working model or a convincing technical demo. The bar for "pre-revenue" has moved — investors in 2026 want to touch something.

Early usage that proves retention, not just acquisition. 100 to 1,000 weekly active users if you're B2C. Three to ten design partners or early customers if you're B2B. The raw user count matters less than the cohort curves — do people come back without you prompting them? Show the cohort table, not the cumulative signup graph.

A team that looks like it can execute. Two co-founders with a credible division of responsibilities. Some evidence of founder-market fit: domain expertise, a relevant network, prior building experience. Solo founders get a harder diligence process and a lower cap. That's not fair, but it's the market.

The materials that let investors say yes fast. A clean 10-slide pitch deck. A three-minute verbal pitch that works without slides. A ranked list of 50 to 100 target investors. Most founders spend weeks on the deck and zero hours on the list — that's backwards.

Related: The Complete Guide to Building a Pitch Deck That Raises Capital

How the Process Actually Works

Most pre-seed rounds in 2026 take three and a half to six months from first meeting to money in the bank. That's roughly double what it was in 2020, and it catches first-time founders off guard every time.

The first month goes to building your target list and getting warm introductions. Cold emails to pre-seed investors have a single-digit response rate. Warm intros from portfolio founders or trusted peers convert at roughly ten times that rate. The fastest way to build a network if you don't have one: attend demo days, reach out to founders who raised from your target investors, and post about what you're building on X or LinkedIn. Serendipity still works.

The next two months are pitch meetings and diligence. Expect three to five meetings per investor — a general partner, an associate, a reference call with an early user, a product demo, and a cap-table model. Investors want to see an 18-month burn plan and understand how this round plus a projected seed round affects everyone's ownership.

When you have a lead committed, the rest of the round usually fills in two to four weeks. Most pre-seed rounds in 2026 close with one lead micro-VC and three to eight angel or rolling fund participants. Announce the round with a narrative, not a press release. Why did these particular investors back you? What does it signal?

The Stat That Should Change Your Strategy

Only 12 to 15 percent of pre-seed startups raise a subsequent seed round, according to Carta's 2024 cohort analysis. For AI startups, the number is higher — roughly 25 percent. For everyone else, it means there is an 85 percent chance your pre-seed round is the only institutional round you will ever raise.

That statistic should change how you think about everything.

Structure your burn so that if seed doesn't materialize, you have a viable path to revenue. Plan for 18 months of runway but aim for product-market fit in 12. Every dollar of MRR you generate during your pre-seed increases your odds of raising a seed by roughly three times. And the investors who write your seed check are almost never the ones you meet for the first time during that process — they're the ones who have been watching your progress for six to twelve months.

Build those relationships during your pre-seed, not after.

Data sources: Carta's 2024 State of Private Markets, PitchBook/NVCA Venture Monitor Q4 2024 and Q1 2025 preliminary data, Cooley GO Annual Report 2024, Y Combinator SAFE documentation, and AngelList rolling fund activity data. All figures are market medians and ranges — your actual terms will vary based on team, traction, sector, and negotiation.

Ready to see how investors would evaluate your pitch? Upload your deck to Bullpen for a free AI-powered assessment across 7 investor categories.

Get weekly pitch tips

One email a week. Actionable advice for founders.

See how investors will grade your pitch. Try now →