Priced Equity Rounds: When to Move Beyond SAFEs

Moving from SAFEs to a priced round is the most consequential financial event in a startup's early life. Here's when it makes sense, what the terms actually mean, and how to avoid the common mistakes that cost founders millions.

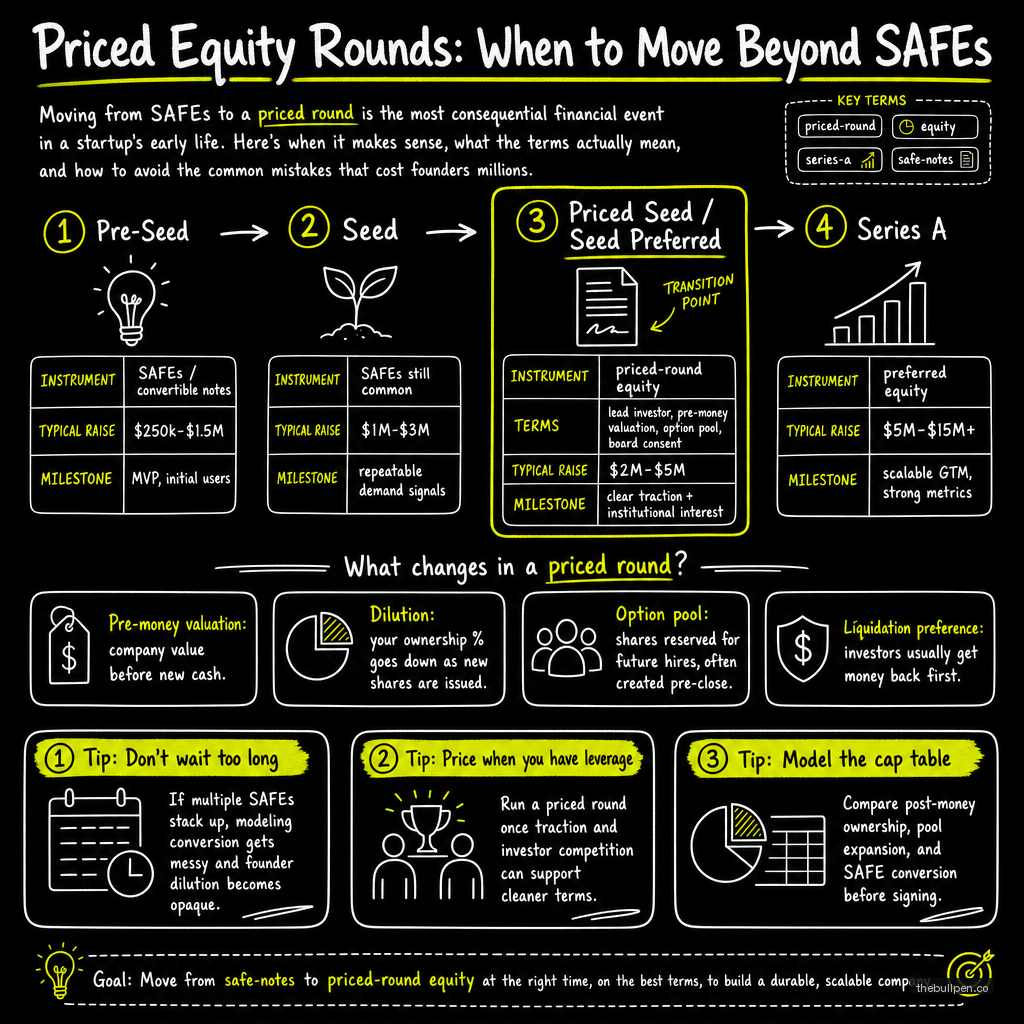

A SAFE is not a round. It's a placeholder. It defers the hard conversation about valuation, board seats, and liquidation preferences to a future date when someone — a Series A lead — is willing to put a price on your company. That future date is called a priced round, and it's the most consequential financial event in your startup's early life.

Most founders don't spend enough time understanding what happens when their SAFEs convert. They know the cap. They know the discount. They don't think about what happens when eight different SAFEs with eight different caps all collapse into a single Series A at the same time, creating a cap table that looks like a plumbing diagram. They don't think about what a 1x participating liquidation preference means if the company sells for less than they hoped. They don't think about anti-dilution mechanics until a down round wipes out half their ownership.

The transition from SAFEs to priced equity is where founder education meets reality. The learning curve is expensive.

Related: The Startup Fundraising Playbook: From Pre-Seed to Series A

SAFE vs. Priced Round: What Actually Changes

The table below captures the structural differences. The important ones aren't the ones most founders focus on.

| Dimension | SAFE | Priced Round (Series A) |

|---|---|---|

| Valuation | Deferred to conversion event | Negotiated and fixed at close |

| Shares issued | None until conversion | Issued immediately |

| Liquidation preference | None (converts into Series A terms) | Yes — typically 1x non-participating |

| Board seats | None | 1 or more for lead investor |

| Information rights | Minimal | Full — monthly/quarterly financials |

| Legal cost | $2,000–$5,000 | $50,000–$150,000 |

| Investor protection | Limited | Full — veto rights, pro-rata, MFN |

| Timeline to close | 1–2 weeks | 3–6 months |

The legal cost jump is the most underestimated line item. A priced round requires a stock purchase agreement, an amended charter, an investors' rights agreement, a right of first refusal agreement, and a voting agreement — each negotiated with experienced VC counsel who bills hourly. Founders who budget $20,000 for legal end up spending $80,000. Founders who budget $80,000 end up spending $150,000.

The Key Terms That Matter

Three terms in a Series A term sheet determine almost everything about the outcome for founders. The rest is noise.

Liquidation Preference

This determines who gets paid first when the company exits. A 1x non-participating preference — the standard for roughly 70% of Series A rounds per Carta's 2024 data — means the investor gets their money back before common shareholders see anything, but they don't double-dip. Once they've recovered their investment, they convert to common and share the rest proportionally.

A 1x participating preference — found in about 25% of Series A rounds — means the investor gets their money back AND then shares in the remaining proceeds. In a moderate exit (say $50 million on $40 million in total investment), participating preferred can shift millions from founders to investors.

The difference between participating and non-participating matters most in the range between 1x and 3x return on investment. Above 3x, the economics converge because converting to common is usually better for the investor anyway.

Anti-Dilution

Weighted average anti-dilution — used in 96% of Series A rounds — adjusts the investor's conversion price if the company raises a down round at a lower valuation. The adjustment is proportional: a down round at 20% below the Series A price triggers a modest adjustment, not a catastrophic one.

Full ratchet anti-dilution, by contrast, resets the investor's price to the lowest price ever paid by any subsequent investor. If you raise a bridge round at half your Series A valuation, full ratchet retroactively rewrites every prior investor's price. It's rare in Series A but appears occasionally when founders have weak negotiating leverage. Never agree to it.

Board Composition

A typical Series A board: two founder seats, one investor seat, and optionally one independent seat. That 3-2 or 3-2-1 structure means the investor can't control the board alone but has a meaningful voice. Founders should fight to keep board control through Series A. Once investors have a majority, the balance of power shifts permanently.

Related: Seed Round Strategy: Raising $1M to $5M in 2026

The Readiness Threshold

The data on when startups raise Series A is well established. Carta's 2024 Series A report tracked over 1,000 rounds and found:

| Metric | 25th Percentile | Median | 75th Percentile |

|---|---|---|---|

| Pre-money valuation | $25M | $60M | $125M |

| Annual Recurring Revenue | $1.0M | $1.7M | $3.2M |

| Round size | — | $10M | — |

| Team size | 10 | 18 | 30 |

The median Series A startup in 2024 had $1.7 million in ARR, an $60 million pre-money valuation, and 18 employees. The $1.7 million ARR threshold is the single most important number to internalize. Below it, your Series A is a harder sell. Above it, you're in range.

But ARR alone doesn't clear the bar. Growth rate matters more. Investors at Series A are looking for 2.5x to 3.5x year-over-year growth, net revenue retention above 100%, gross margins above 60% (70%+ for SaaS), and a burn multiple under 2x — meaning for every dollar of ARR added, you burn less than two dollars.

How SAFEs Actually Convert

The mechanics of SAFE conversion surprise most founders. When you raise a Series A, all outstanding SAFEs convert into Series A preferred stock at the same time. The conversion price for each SAFE is the lower of:

- The price implied by the SAFE's valuation cap divided by fully diluted shares

- The Series A price per share discounted by the SAFE's discount rate (typically 15-25%)

A SAFE with a $5 million cap and a 20% discount on a $10 million Series A pre-money converts as if the company were valued at $5 million — roughly twice the shares per dollar as the Series A investors. The cap protects the early investor. The discount rewards them for investing early. Both apply, and the more favorable one is used.

The problem arises when SAFEs have widely varying caps. A $20 million cap SAFE and a $5 million cap SAFE produce very different conversion ratios. When they all collapse into the same Series A, the cap table gets complicated fast. Founders who raise SAFEs at incrementally increasing caps — $5M, $8M, $12M, $20M — create a waterfall that's expensive to model and even more expensive to explain to a Series A lead.

Related: SAFE Notes vs Convertible Notes: Which One Should You Use?

When to Make the Move

The decision to raise a priced round comes down to one question: is the clarity of a fixed valuation worth the complexity and cost?

| Raise a Priced Round When | Stay on SAFEs When |

|---|---|

| You have $1M+ ARR and clear growth trajectory | Revenue is doubling every 3 months (you'll get a much better price in 6 months) |

| You need $5M+ to hit your next milestone | You're raising less than $2M (legal costs eat too much) |

| You want institutional investors on the cap table | Market conditions in your sector are unfavorable |

| You need the governance and board guidance of a lead investor | You need to hit a product milestone first |

| Your SAFE caps are getting too high for the next round | Your cap table is too messy to resolve cleanly |

The general rule: if you can raise a priced round at a valuation that feels fair relative to where you'll be in nine months, take it. If you're confident you'll triple ARR in six months, stay on SAFEs and raise when that happens. Figma raised multiple SAFE rounds before their eventual priced round at a $2 billion valuation. Gusto extended seed-stage financing for 18 months. The cost of waiting is uncertainty. The reward is a higher valuation and less dilution.

The Bottom Line

A priced round is fundamentally different from everything that came before it. SAFEs are simple, fast, and founder-friendly. Priced rounds are complex, slow, and lawyer-intensive. The transition marks the moment when your company goes from "experiment with potential" to "institutional-grade investment."

The mistake founders make is treating the priced round as a milestone to check off rather than a structural change in how the company is governed. Once you have a Series A lead with a board seat, a liquidation preference, and information rights, you're not operating the same company you were before. The additional capital comes with constraints.

Know the terms. Know the timing. And know that the best time to understand a liquidation preference is before you sign the term sheet, not after.

Published on the Bullpen Blog. New articles every day at 9 AM UTC.

Get weekly pitch tips

One email a week. Actionable advice for founders.

See how investors will grade your pitch. Try now →