Financial Projections in a Pitch Deck: How Far Is Too Far?

The art of presenting financial projections in a pitch deck — how to show ambition without destroying credibility, and what investors actually look for at each stage.

Most founders project $50M in revenue by year three. Most founders will never see $50M in revenue, period. The gap between those two statements is where your credibility lives or dies.

Investors do not expect you to predict the future. They expect you to understand your business well enough to make educated assumptions about where it's going. Those are different skills. One requires humility. The other requires spreadsheets.

The tension is real: show too little ambition and you seem like you're building a lifestyle business. Show too much and you look naive. DocSend analyzed how much time investors actually spend on financial projection slides. The number is 89 seconds — roughly half the time they spend on traction. In those 89 seconds, they decide whether you understand your own business model well enough to trust with their capital. Most founders bomb this test because they confuse volume of numbers with quality of thinking.

Related: The Complete Guide to Building a Pitch Deck That Raises Capital

The Hockey Stick Problem

Every investor has seen the chart. Year one: $500K. Year two: $5M. Year three: $50M. The line goes up and to the right at a forty-five-degree angle that would impress a NASA trajectory engineer.

That chart is why your projections are not credible.

The "hockey stick" is not inherently wrong. Some companies do grow that fast. Stripe went from zero to billions in under a decade. But Stripe's deck did not show that trajectory in year one — it showed the logic that made that trajectory possible. The difference is critical.

Investors see thousands of decks per year. They have developed a finely tuned detector for projections that were built backward from a target number. "We need to raise $5M at a $20M valuation, so we need to show $50M in revenue by year five" is a common thought process. It is also completely transparent to anyone who has funded a startup.

Buffer's seed deck handled this differently. Instead of projecting three years out, they showed $5K MRR with 11% weekly growth and let the math speak. They did not claim they would be at $50M in three years. They showed the current trajectory and the unit economics that made acceleration plausible. The projections were anchored in something real: the growth rate they had already demonstrated.

DocSend's eye-tracking study confirmed that investors who spend more than 89 seconds on financial slides are not checking your revenue projections for accuracy. They are checking your assumptions. They want to see whether you have thought through the drivers — not just the outputs.

Related: The Problem Slide: Why Most Founders Rush It (And Why You Shouldn't)

What Belongs on the Slide vs What Goes in the Appendix

The financials slide in the main deck is not a P&L statement. It is a summary of the key assumptions that drive your business. Everything else goes in the appendix.

Dropbox's early fundraising materials are instructive here. When Drew Houston pitched Y Combinator, his financial slide was almost laughably simple by today's standards: a single table showing user growth projections and a unit economics breakdown. No three-statement model. No balance sheet. No cash flow statement. He showed the one thing that mattered — the unit math of acquiring a user and converting them to paid — and let the scale do the rest.

Compare that to the average founder's deck today. A full income statement projected five years out. A balance sheet with line items for prepaid expenses and deferred tax assets. A cash flow statement that somehow shows positive cash flow in year two for a company that has not launched yet. None of this inspires confidence. It inspires suspicion.

The rules are simple. The main deck financial slide gets three things: the revenue build (what drives growth), the unit economics (what makes each customer profitable), and the path to breakeven (when you stop burning cash). Everything else — the expense detail, the headcount build, the balance sheet — goes in the appendix. Investors who want it will ask. Investors who do not want it will be annoyed you wasted slide space on it.

Uber's Series A deck had a single "Financial Summary" slide. It showed projected rides, revenue per ride, gross margin, and EBITDA. Four numbers. No line items for driver acquisition costs or insurance reserves. Those details lived in the appendix. The main slide told the story. The appendix proved the math.

Related: How to Write a One-Liner That Makes Investors Want to Read More

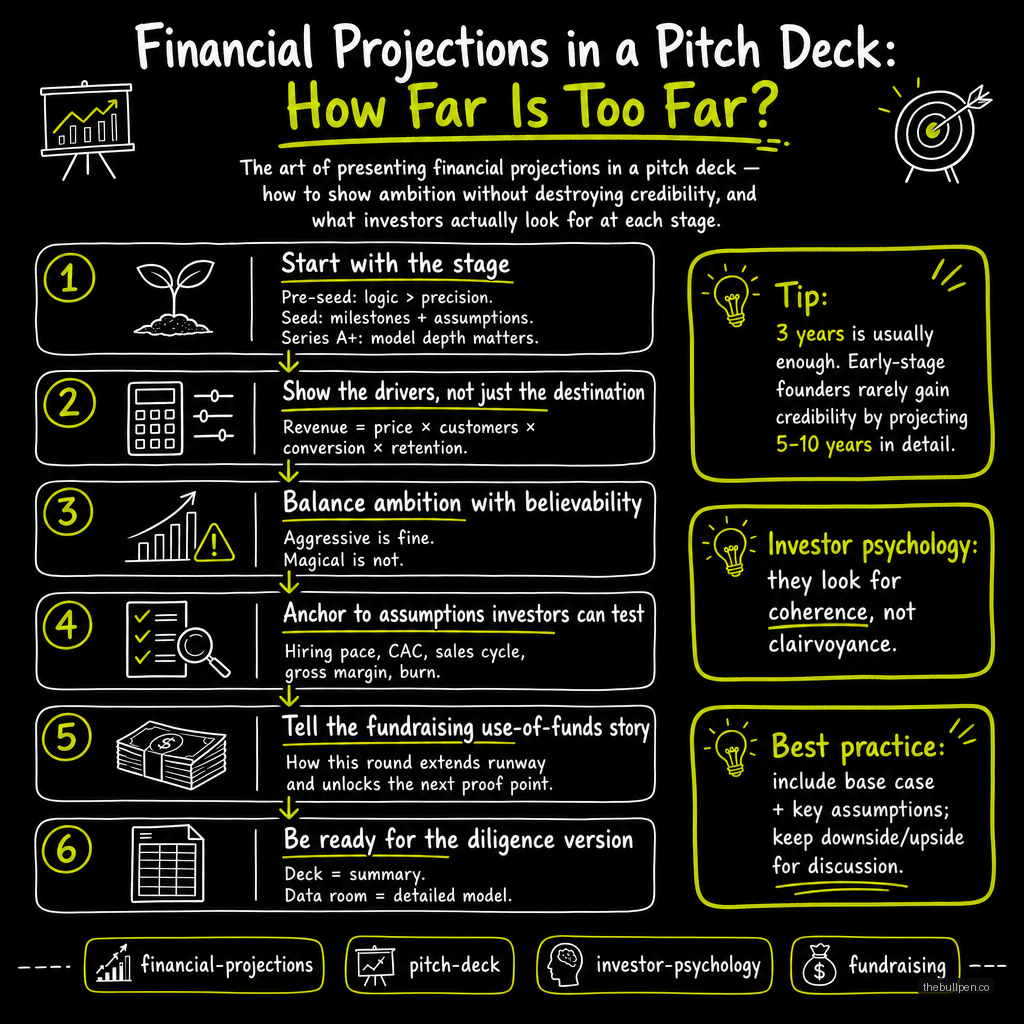

What to Show at Each Stage

The financial projections that work at pre-seed are different from what works at Series A. Using the wrong level of detail makes you look either overconfident or unprepared.

Pre-seed: unit economics only. You do not have revenue. You may not have a product. The only financial projections that matter at this stage are the unit economics that prove your business model. What is the expected customer acquisition cost? What is the expected lifetime value? What is the gross margin on each transaction? These are not predictions — they are hypotheses. Show you understand the math of your business.

Airbnb's YC demo day deck did not show a five-year P&L. It showed the economics of a single booking: the average rental price, the platform's take rate, and the implied margins. Three numbers that proved the business model worked at a unit level. The assumption was that if each transaction was profitable and the marketplace was growing, the aggregate numbers would follow.

Seed stage: growth trajectory plus retention. You have some revenue. You have real users. Your projections need to show that you understand what is driving growth and whether it can continue. The headline number is MRR or ARR trajectory with a growth rate. The second number is retention — monthly cohort retention, net revenue retention, or both.

Buffer showed $5K MRR and 11% weekly growth. They also showed 92% monthly retention. The growth rate explained why they would be big. The retention rate explained why they would stay big. Those two numbers together are more powerful than any three-statement model.

Series A: full P&L with retention curves. By this point you have twelve to eighteen months of operating history. You can project revenue with reasonable confidence because you have seen the cohort curves stabilize. Your financials slide should show a complete P&L — revenue, COGS, gross margin, operating expenses, and EBITDA — projected three years out. Back it with cohort retention curves that validate your growth assumptions.

The key difference between a good Series A financial slide and a bad one is how you handle the unknowns. The best decks show three scenarios that bracket the range of outcomes. The worst decks show one scenario and imply it is inevitable.

Related: Traction Slide Examples: What Seed-Stage Investors Actually Want to See

The Three-Scenarios Approach

The single most effective way to present financial projections — and the one most founders skip — is the three-scenario model.

Conservative. What happens if growth plateaus? If retention drops by ten points? If the market takes longer to develop than expected? This scenario shows that you can survive the downside. It does not need to be pretty. It needs to show that the business does not die.

Base case. What happens if current trends continue? This is your operating plan. It should be ambitious enough to justify the fundraise but grounded enough to be plausible. The base case is the one you reference in board meetings.

Ambitious. What happens if everything goes right? This is the scenario that makes investors dream. It should show the size of the opportunity without making claims about your ability to execute. The difference between the ambitious case and the base case should come from market tailwinds and product-market fit acceleration — not from random assumptions you pulled from a benchmark report.

The three-scenario model serves two purposes. It signals that you understand uncertainty — a sign of founder maturity that investors value more than any single projection. And it gives investors a framework to debate your business without attacking your credibility. An investor who disagrees with your growth assumption can say "I think the base case is too aggressive" instead of "I don't trust your numbers." The conversation stays productive.

Related: Seed Round Strategy: Raising $1M-$5M in 2026

What the Numbers Actually Say About Your Business

There is a pattern in how experienced investors read financial projections. They do not look at year five. They look at year two.

The reason is simple: year five projections are fiction. Too many variables change in sixty months. But year two tells you whether the founder understands the next milestone. If your year-two numbers do not match the capital you are raising — if you are raising $5M but projecting only $500K in year-two revenue — there is a mismatch that needs explaining.

The second thing investors check is gross margin trajectory. If your gross margin stays flat for five years, you are not building a software business — you are building a services business with a software wrapper. Software gross margins should improve over time as you amortize fixed costs across a growing customer base. If yours do not, you either have a structural problem or you have not thought through your cost drivers.

The third thing is the relationship between headcount and revenue. Most decks show headcount growing linearly while revenue grows exponentially. That works on paper. In practice, adding people adds complexity faster than it adds output. If your headcount-to-revenue ratio implies that each new hire generates $500K in revenue in year three, you are either hiring only salespeople or your model is wrong.

Related: Series A Preparation: What VCs Actually Look For

What to Cut Right Now

Open your financial projections file. Find the sheet that projects five years out. Delete it.

You do not need it. Year four and five projections add no signal. They add noise. Every assumption you make for year four compounds errors from years one, two, and three. The error bars are so wide that the numbers are meaninglessly precise. Investors know this. They ignore year five anyway. Remove the vanity and focus the space on what actually matters.

Then cut the detailed expense breakdown. Your investors do not need to see line items for office supplies, software subscriptions, and travel expenses. They want to know your biggest cost drivers — headcount, infrastructure, and customer acquisition — and how those scale. The granular budget belongs in your operating plan, not your pitch deck.

Replace what you cut with two things: a clear statement of your key assumptions and the sensitivity analysis that shows how changes in those assumptions affect the outcome. If your business depends on a specific cost-per-lead remaining below $50, say it. If your model breaks if churn goes above 5%, show the math. The goal is not to prove you are right. It is to prove you have thought about what could go wrong.

Buffer's most-transparent moment was not any projection. It was founder Joel Gascoigne publishing their actual numbers every month and letting the market validate their trajectory. The result was a compounding of trust that no three-statement model could match.

The founders who raise capital have projections. The founders who raise capital on good terms have projections that survive the first five minutes of scrutiny. The difference is not in the numbers. It is in the assumptions behind them. Build those well, and the numbers take care of themselves.

Data sources: DocSend 2018 Pitch Deck Study (investor time spent per slide), Dropbox YC application materials, Buffer's transparent revenue data published by Joel Gascoigne, Airbnb YC W09 seed deck (analyzed by Slidebean/Business Insider), Uber Series A pitch deck (2011).

Ready to see how investors would evaluate your pitch deck's financial projections? Upload your deck to Bullpen for a free AI-powered assessment across 7 investor categories.

Get weekly pitch tips

One email a week. Actionable advice for founders.

Upload your deck. Get scored in 2 minutes. Free. Try now →