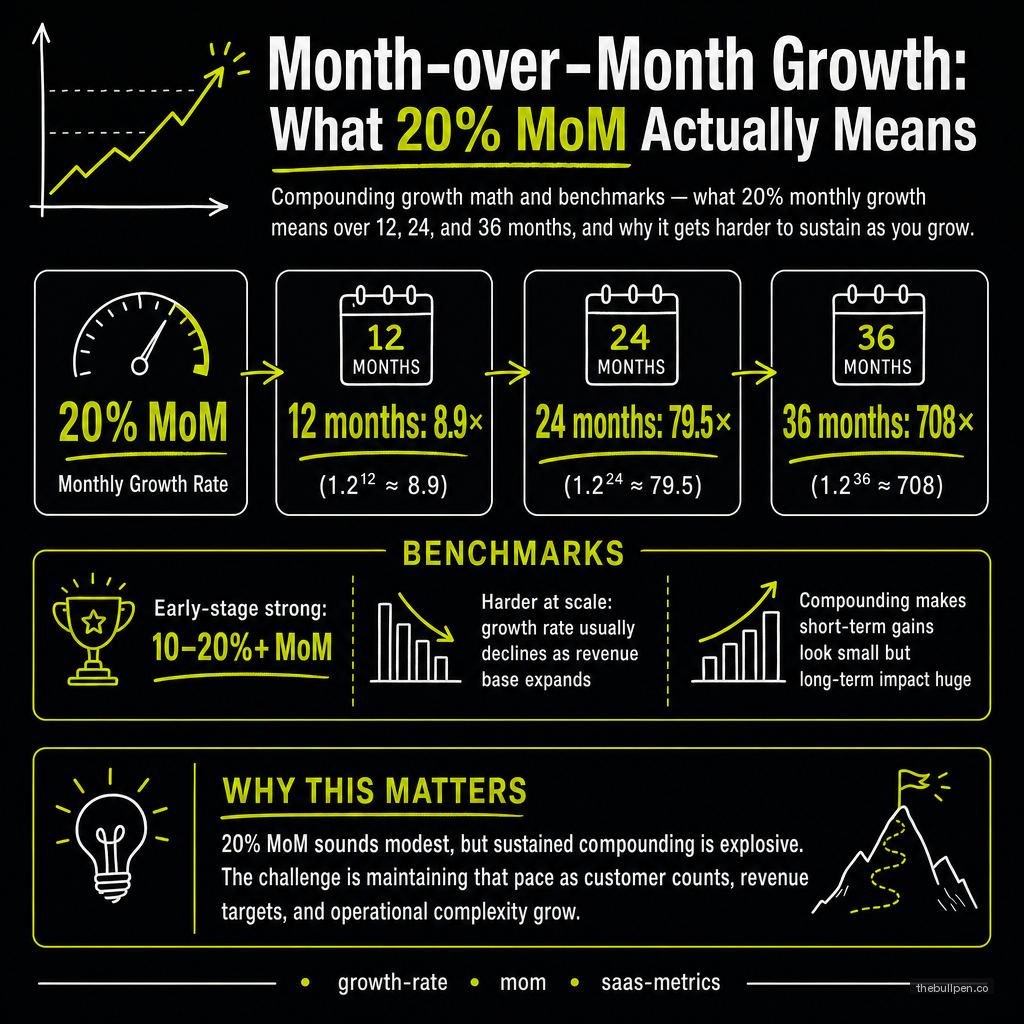

Month-over-Month Growth: What 20% MoM Actually Means

Compounding growth math and benchmarks — what 20% monthly growth means over 12, 24, and 36 months, and why it gets harder to sustain as you grow.

Month-over-Month Growth: What 20% MoM Actually Means

Twenty percent month-over-month growth sounds like a vanity number. A line that goes up. A stat you put in a pitch deck alongside a hockey-stick chart and hope a venture partner doesn't squint too hard. But 20% MoM is one of the most misunderstood metrics in early-stage SaaS. It's simultaneously the most powerful growth rate a startup can achieve and the fastest way to burn through your credibility if you don't understand what it actually demands.

Here's what 20% MoM really means — in dollars, in time, in retention, and in stage-appropriate context.

The Compounding Is Not Linear

A startup growing 20% month over month is not growing 240% per year. It's growing a lot more than that. Compounding at this rate produces results that feel wrong until you run the math yourself.

Start with $10,000 in monthly recurring revenue. Apply 20% MoM growth and track what happens.

| Month | MRR | ARR (Run-Rate) |

|---|---|---|

| 1 | $10,000 | $120,000 |

| 3 | $17,280 | $207,360 |

| 6 | $29,860 | $358,320 |

| 9 | $51,597 | $619,164 |

| 12 | $89,161 | $1,069,932 |

| 18 | $266,233 | $3,194,796 |

| 24 | $794,969 | $9,539,628 |

That $10K MRR becomes $89K MRR by month 12 — nearly nine-fold growth in a single year. By month 24, you're pushing $795K MRR and a run-rate of $9.5 million ARR. From ten grand.

The Rule of 72 puts a finer point on it. Divide 72 by 20 (your growth rate) and you get 3.6. That's the number of months it takes to double at 20% MoM. You double once per quarter. Eight doublings in two years. That's the arithmetic that makes VCs sit up straight — and why experienced operators look at 20% MoM with a mix of excitement and skepticism.

The excitement comes from the math. The skepticism comes from knowing how hard it is to keep compounding through scale, churn, and market saturation.

Related: Growth Accounting in SaaS

Why 20% Means Different Things at Different Stages

The context that matters most is stage. Twenty percent MoM at $5K MRR is table stakes. Twenty percent MoM at $500K MRR is exceptional. Twenty percent MoM at $5M MRR is almost unheard of.

Here are the benchmarks used by the top venture firms to evaluate growth quality by stage:

| Stage | Good | Great | Implied MoM Deceleration |

|---|---|---|---|

| Seed ($0–$100K MRR) | 15–20% | 25%+ | None expected yet |

| Series A ($100K–$1M MRR) | 10–15% | 15–20% | ~5% per year |

| Series B ($1M–$5M MRR) | 7–12% | 12–15% | ~3–5% per year |

| Public ($10M+ MRR) | 3–5% | 5–7% | ~1–2% per year |

A seed-stage company growing 20% MoM is on a great trajectory. A Series A company maintaining 20% MoM is a top-quartile outlier. A public company growing 20% monthly would be doubling revenue every 3.6 months — something no public SaaS company has ever done at scale.

Paul Graham captured the logic that underpins these expectations: "Growth rate is the only thing that matters." He advised Y Combinator founders to target 5–7% weekly growth in the earliest days. Monthly 20% is roughly the decelerated version of that weekly velocity , a signal that product-market fit is real and the engine is turning.

The key insight here is that growth deceleration is normal and baked into every stage transition. The question isn't whether your MoM rate drops , it's whether it drops on schedule or falls off a cliff.

Related: SaaS Metrics Every Founder Should Track

The Churn Tax Few Founders Model Correctly

Here's where the math gets painful. Twenty percent gross MoM growth means nothing if customers are leaving at the same time.

Imagine you're adding 20% new MRR every month, but you're losing 5% of existing MRR to churn. Your net growth rate isn't 20% . it's approximately (1.20 × 0.95) − 1 = 14%. Every month you lose a fifth of your gains to leakage.

Run that same $10K MRR scenario with the churn-adjusted 14% net growth rate:

- Month 12 MRR (with churn): ~$48,000

- Month 12 MRR (without churn): ~$89,000

That's a $41,000 difference , nearly half your revenue gone. Over 24 months the gap widens to hundreds of thousands of dollars in missed MRR.

This is the difference between the spreadsheet startup and the real one. In a deck, 20% gross growth looks heroic. On a P&L, 5% monthly churn plus 20% gross growth produces a 14% net number that might not impress a Series A partner whose bar is 15%.

The growth rate matrix makes this concrete:

- High Growth + High Retention = Unicorn potential. The classic efficient growth story that SaaS investors love.

- High Growth + Low Retention = Leaky bucket. You're spending acquisition dollars to fill a bathtub without a drain plug. Unit economics will eventually catch up.

- Low Growth + High Retention = Slow climb. Often a profitable lifestyle business, but not venture-backable at scale.

- Low Growth + Low Retention = Dead end. Fix product-market fit before touching growth levers.

Real companies that sustained high MoM did it with retention as the foundation. Facebook held roughly 20% monthly growth for 18 months straight , but also had near-zero churn because network effects created lock-in. Slack ran ~14% MoM for 24 months with some of the lowest churn numbers in enterprise SaaS history. Zoom hit ~15% MoM over 24 months with a product so sticky that churn was essentially an afterthought. Uber maintained ~18% MoM for 30 months, powered by marketplace retention loops on both the rider and driver sides.

In every case, the raw growth number was impressive. But the retention underneath is what made it durable.

Related: Net Revenue Retention: The Metric Behind Efficient Growth

What 20% MoM Demands from Operations

Sustaining 20% MoM means your company is roughly doubling every quarter. That kind of compounding turns a financial milestone into an operational gauntlet.

Customer support needs to scale at the same rate. Infrastructure has to handle 1.2× the load every thirty days. Hiring needs to keep pace, which means recruiting, onboarding, and culture all get compressed into impossible timelines. Product development needs to ship features fast enough to keep the growth engine running while also paying down technical debt that accumulates geometrically.

This is why most startups that hit 20% MoM don't stay there for long. Not because the market dries up, but because the organization can't absorb that rate of change.

The companies that do sustain it share a pattern: they invest early in systems and process. They hire generalists who can handle scope expansion. They build for scale before scale arrives. And they track retention metrics with the same intensity as growth metrics , because they know that 20% MoM without retention is just a faster path to the same dead end.

Twenty percent MoM is the upper bound of sustainable growth for most venture-backed startups. It's the number that separates good companies from generational ones. But it's also a number that demands respect , for the compounding math that makes it powerful, for the retention dynamics that make it real, and for the operational strain that makes it rare.

Published on the Bullpen Blog. New articles every day at 9 AM UTC.

Get weekly pitch tips

One email a week. Actionable advice for founders.

Benchmark your metrics against investor expectations. Try now →