Burn Multiple: The Metric That Tells You If You're Dying Efficiently

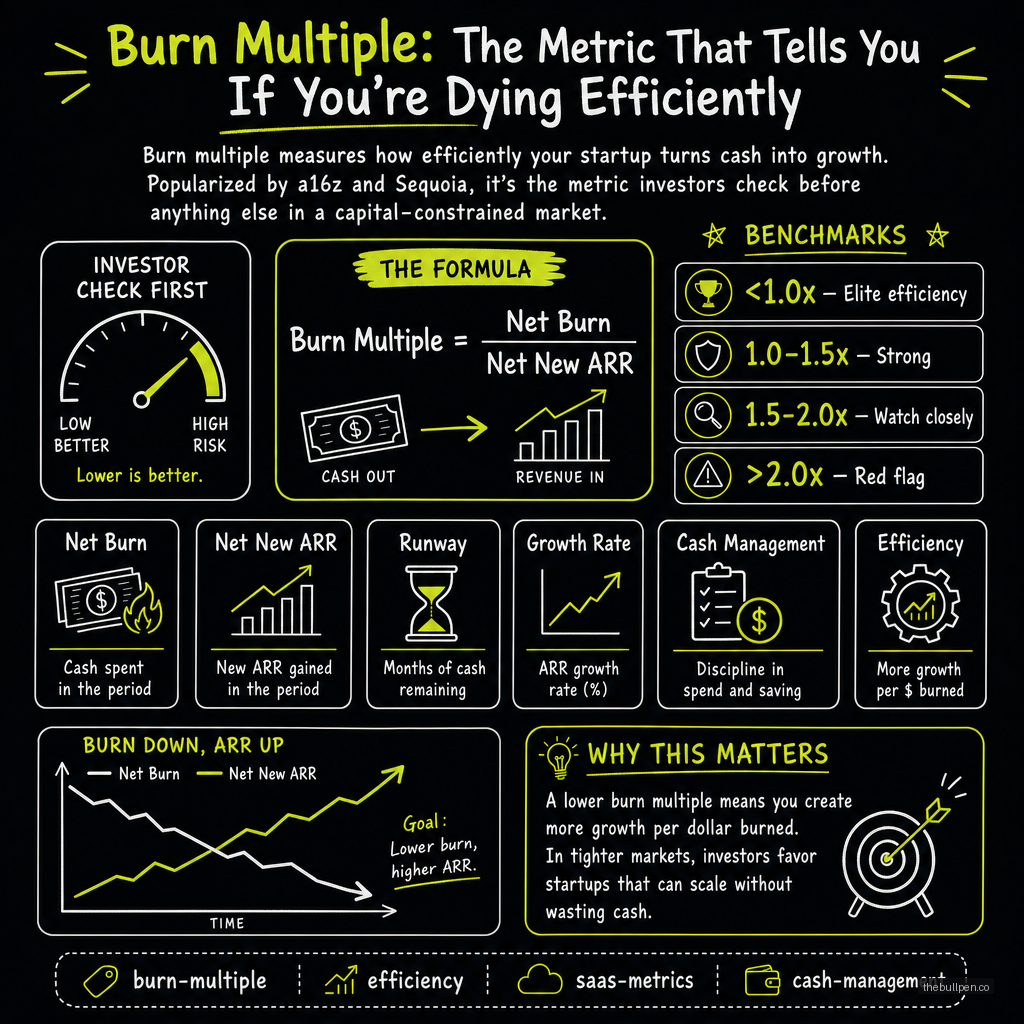

Burn multiple measures how efficiently your startup turns cash into growth. Popularized by a16z and Sequoia, it's the metric investors check before anything else in a capital-constrained market.

There's a metric that tells investors more about your startup's health than growth rate, revenue, or market size. It's not reported on your P&L. It's not in your GAAP financials. But a16z uses it. Sequoia uses it. And if you're raising in a capital-constrained environment, they're looking at yours before anything else.

Burn multiple measures how much cash you spend to generate each dollar of net new recurring revenue. The formula is:

Burn Multiple = Net Burn / Net New ARR

If you burn $5M in a quarter and add $2.5M in net new ARR, your burn multiple is 2.0x. You're spending $2 to get $1 of new recurring revenue per year. If you burn $3M and add $3M in ARR, your burn multiple is 1.0x — spending $1 to get $1.

The lower the number, the more efficient your growth. In the zero-interest-rate era, a 5x burn multiple was acceptable if growth was fast enough. Today, 3x is a warning sign and anything above that is a crisis.

Related: Startup Metrics That Matter: What Investors Actually Look For

The Benchmarks

| Burn Multiple | Rating | Meaning |

|---|---|---|

| Below 1x | Exceptional | Nearly capital-efficient — each dollar of spend generates over a dollar of ARR |

| 1x to 2x | Good | Healthy efficiency for a growth-stage company |

| 2x to 3x | Caution | Over-spending. Needs improvement within 2 quarters |

| Above 3x | Dangerous | Structural problem. Will run out of cash before the model works |

The metric varies by stage. Pre-seed companies often have a burn multiple below 1x because headcount is low and ARR grows quickly off a small base. Series A companies typically climb to 1.5x-2.5x as they build GTM teams. Series B companies should trend back to 1x-2x as efficiency improves. A Series B company with a 3x+ burn multiple has unit economic problems.

Sequoia's famous "R.I.P. Good Times" presentation explicitly flagged burn multiple as the metric separating survivors from casualties. Companies above 3x were told to cut burn or raise immediately.

Why It Matters More Than Growth Rate

Growth rate tells how fast you're going. Burn multiple tells how long you can keep going.

A startup growing 200% per year with a 5x burn multiple is exciting until you do the math. They're spending $5 to generate $1 of new ARR. If they have $10M in the bank and are burning $2M per month, adding $400K in new ARR per month, they'll be out of money in five months. The growth rate is meaningless if the burn multiple is unsustainable.

A startup growing 50% per year with a 1.2x burn multiple can keep growing for years without additional capital. They're spending $1.20 to generate $1 of new ARR. The cash lasts longer. The model is proven. Investors will fund this company because the risk is lower.

| Scenario | Growth Rate | Burn Multiple | Verdict |

|---|---|---|---|

| Startup A | 200% YoY | 5.0x | Exciting but fragile — will need cash soon |

| Startup B | 80% YoY | 1.5x | Healthy — capital-efficient growth |

| Startup C | 50% YoY | 0.8x | Exceptional — nearly profitable |

Related: Net Revenue Retention: The Metric That Predicts Startup Success

How to Improve It

Increase pricing. Most early-stage startups underprice. A 20% price increase adds directly to ARR without increasing burn. It's the single most efficient lever.

Improve sales conversion. Better demos, better targeting, better qualification. Every improvement in conversion rate reduces CAC and improves burn multiple without cutting spend.

Cut low-ROI channels. Most startups have at least one marketing channel losing money. Kill it. The ARR won't drop proportionally because those customers had the highest CAC and lowest retention.

Control headcount growth. Headcount is the biggest driver of burn. Add people only when there's clear evidence that the new hire generates more revenue than they cost.

Grow existing customers. Expansion revenue has near-zero acquisition cost. Every dollar of expansion MRR improves burn multiple without any incremental spend. Companies with NRR above 120% naturally have better burn multiples.

When to Worry

If your burn multiple has been above 3x for two consecutive quarters, you have a structural problem. The model needs to change — pricing, GTM strategy, or product. More capital will not fix a 5x burn multiple. It will just delay the reckoning.

The companies that failed in the 2022-2023 correction — WeWork at 4.5x+, Bird and Lime above 5x, Cazoo at 7x — all had the same problem. The growth story was compelling until investors asked how much it cost. When the answer was more than the revenue with no path to efficiency, the capital dried up.

Track burn multiple quarterly. Set a target under 2x. And if you see it trending the wrong way, act before your investors force you to.

Published on the Bullpen Blog. New articles every day at 9 AM UTC.

Get weekly pitch tips

One email a week. Actionable advice for founders.

Benchmark your metrics against investor expectations. Try now →